U.S. Review

Geopolitical Developments Ring in the New Year

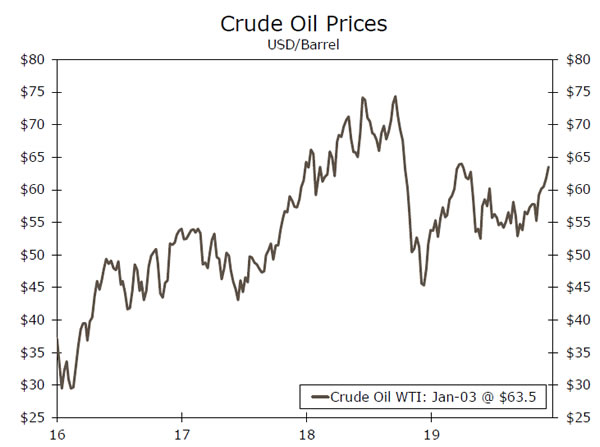

- It was a light week for economic data in a shortened holiday week. But, news of President Trump ordering an airstrike in Iraq and killing a top Iranian military general resulted in a riskoff response from markets as oil prices surged and Treasury yields fell early Friday morning.

- Markets were also pressured from the latest ISM manufacturing report, which signaled further deterioration in the sector with the index falling to its lowest level since 2009.

- The Conference Board reported a decrease in consumer confidence for the final month of the year, but we continue to see strong consumer fundamentals.

Geopolitical Developments Ring in the New Year

There were two notable geopolitical developments that grasped markets attention this week. First, President Trump announced that the Phase I trade deal with China will be signed in the White House on January 15, which should provide its detailed terms. Second, and more prominent, Trump ordered an airstrike in Iraq that resulted in the killing of Qassem Soleimani, one of Iran’s top military generals. Oil prices jumped and Treasury yields fell on the news. The largest macro concern beyond yet more geopolitical uncertainty is the lasting impact to oil prices, which will depend on if/how Iran responds.

Turning back to trade—while the Phase I deal was officially announced on December 13, this week’s statement of its forthcoming signing was seen as more than a formality for markets. Rumblings of a possible Phase I deal have been anticipated for months, but the actual passage of the deal exemplifies the first true de-escalation in the trade war. The deal slashed tariffs in half on approximately $120B of imports from China and dismissed the 15% tariff on an additional $156B, which was set to go into effect just days after being announced. On January 15, we expect to receive more detailed terms of the deal.

While the deal should certainly provide some lift to confidence, with approximately 70% of imports from China still exposed to tariffs a resurgence in business activity remains unlikely. Indeed, consumer and business optimism wobbled last year, not just due to additional tariffs being levied but as a result of the unpredictable nature of the trade environment. The Phase I deal is a step in the right direction, but does not provide solace to manufacturers who may still be exposed to tariffs or now recognize tariffs could be used as a geopolitical tool again in the future. As such, we expect investment spending to remain subdued this year.

The latest ISM manufacturing survey showed the ISM manufacturing index declined to 47.2 in December—the lowest since 2009. Various subcomponents of the index also plumbed lows that haven’t been touched in a decade. The trade war has certainly weighed on the sector, but the downward momentum in the ISM has been decidedly worse than other purchasing manager surveys. A continued de-escalation in trade tensions would be a welcome development for manufacturing. But, the temporary suspension of Boeings’ 737 MAX production is an additional headwind for the sector in the near-term.

Consumers’ confidence dipped in December, but at 126.5 the Conference Board index treaded modestly above its average monthly read of the year (126.2). Consumers were wary last year amid trade uncertainty and recession fears, but there is arguably some upside to confidence in the near term. The cutoff date for last month’s survey was December 13—the same day the Phase I trade deal was announced—meaning optimism from the deal was likely not fully captured in December. Furthermore, with the deal set to be signed mid-January, we may get some upswing in next month’s index. More broadly, low inflation, continued gains in the stock market and a healthy labor market should continue to bolster consumer optimism—and therefore spending—in the new year.

U.S. Outlook

Trade Balance • Tuesday

Monday morning’s trade balance report will command more attention than usual due to the surprisingly large drop reported in the advance goods trade report. The advance goods trade deficit shrank $3.6 billion in November and came in around $5 billion below expectations. Apparently, attempts by U.S. businesses and Chinese producers to keep a step ahead of tariffs led to a surge in imports in August and the past three months have seen imports tumble at a 13% annual rate. While some of that slide in imports has been offset by less inventory building, the decline in imports will likely lead to a larger-than-expected improvement in the trade deficit during the fourth quarter and boost estimates for fourth quarter real GDP growth. The advance report has been a fairly good predictor of the goods portion of the international trade report, so a substantial improvement is now widely expected.

Previous: -$47.2 billion Wells Fargo: -$43.3 billion Consensus: – $45.0 billion

ISM Non-manufacturing Index • Tuesday

While the ISM non-manufacturing survey has held up better than its more widely watched manufacturing counterpart, there is likely to be a great deal of focus on the non-manufacturing survey this week. The overall index has averaged just 53.7 over the past three months and remains near its recent lows. The new orders series, which is one of the leading components of the survey, has risen for the past two months and is back to 57.1, which is slightly above the average for the past six months but still below the trailing 12-month average. Further improvement here would be a positive sign and suggest the recent lull in economic growth is behind us. Most of the attention will be on the employment components, however, which are a key input into many nonfarm employment forecasts. The survey’s employment series has risen solidly for the past two months–closely corresponding with the surprisingly good jobs data.

Previous: 53.9 Wells Fargo: 54.3 Consensus: 54.5

Nonfarm Employment • Friday

We expect Nonfarm payrolls to rise by 160,000 in December, following November’s blowout 266,000-job gain. As noted earlier, employment forecasts may change a bit before the data are released depending upon what is reported in the ISM surveys and possibly the ADP employment report, which has not shown anywhere near as much strength as the BLS data have.

The employment report is full of interesting details that provide insight into many areas of the economy. The manufacturing data have been more volatile of late due to the earlier strike at GM and return of striking workers in the November data. Amidst this noise, the diffusion index, which measures the share of manufacturing industries adding jobs, has been gradually improving, hinting that the manufacturing slowdown may be coming to an end. The household data for 2019 will also be revised to new population estimate and seasonal factors.

Previous: 266K Wells Fargo: 160K Consensus: 163K

Global Review

China Showing Signs of Stabilization

- China’s economic activity and PMI data have improved and beat consensus forecasts in November and December. While we continue to believe China’s economy will decelerate in the coming years, a Phase I trade deal and reduction to the reserve requirement ratio for Chinese banks should provide some support to China’s economy.

- Chile’s economy continues to be disrupted by political protests, with the most recent data indicating the economy contracted for the second consecutive month. Given the updated data, it is likely Chile’s economy contracted in Q4-2019 and could fall into technical recession in 2020.

China Data Improving; PBoC Continues to Ease

For the majority of 2019, Chinese economic data were underwhelming, highlighting a continued slowdown in China’s economy. We can point to persistent trade tensions with the United States as a reason for the lackluster economic data; however, more structural imbalances are also likely a contributor to China’s deceleration. The past few months of the year proved to be much better for China’s prospects heading into 2020, as economic data and sentiment indicators improved to close out 2019. Late last year, the possibility of a Phase I trade deal with the U.S. likely alleviated some pressure on the economy, helping industrial output and retail sales not only improve but beat consensus forecasts in November. In addition, the December manufacturing PMI was released this week and indicated sentiment in the manufacturing sector held steady at 50.2 despite market participants forecasting a mild softening. With a Phase I trade deal now agreed upon and likely to be signed in mid-January, we would expect these activity and sentiment indicators to continue to show modest improvement in early 2020 and ultimately provide some support to China’s economy.

Despite the recent data improvement, the Peoples Bank of China (PBoC) acted again to ease monetary policy this week. The PBoC lowered its reserve requirement ratio (RRR) for all domestic banks another 50 bps, which is set to take effect January 6th. The reduction will take the RRR for major banks to 12.50% and for smaller banks the RRR will be reduced to 10.50%. By easing reserve requirements for Chinese banks, the PBoC will release close to CNY800B of liquidity into the local financial system. This additional liquidity should be supportive of household borrowing and ultimately should provide further support to China’s economy. The PBoC has aggressively lowered the RRR for both big and small banks, dropping the rate 900 bps respectively since the end of 2011. Looking ahead, we expect the PBoC to continue to maintain an accommodative monetary policy stance and expect further reductions to RRR in an effort to support the country’s growth prospects.

Protests Still Hurting Chile’s Economy

Chile’s economy came under pressure in 2019 as anti-government protests spread across the country. Protests forced businesses to close and disrupted transportation resulting in economic activity contracting sharply in October. Data on economic activity suggested that Chile’s economy contracted for the second consecutive month, declining 3.3% year-over-year in November. The economic activity index is typically a good indicator of GDP growth, and with contractions in both October and November, it is likely that Chile’s economy contracted in the fourth quarter of 2019. As a result of the downturn in the economy, the government has implemented a fiscal stimulus plan to help revive the economy, while the central bank moved forward with an FX intervention program to stabilize the currency. Looking forward, we expect the economy to remain under pressure, while the probability of Chile falling into technical recession is high.

Global Outlook

Eurozone Retail Sales • Tuesday

Eurozone retail sales dropped 0.6% on a sequential basis in October, the second-straight monthly decline, while the year-over-year trend appears to have flattened out as well. Based on sentiment data, sales may have remained soft over the remainder of Q4, as the services PMI averaged just 52.4 during the quarter, down from 52.8 in Q3. Next week’s release of November retail sales data will offer more insight into how the hard consumer data fared during the month. On the whole, we expect private consumption growth to have slowed sharply in Q4 after 0.5% sequential growth in Q3. Fortunately, most consumer indicators suggest the slowdown in spending will be fairly short lived. Indeed, disposable income growth remains fairly robust and inflation is contained, while the labor market has been resilient despite ongoing weakness in goods-producing sectors of the economy. Accordingly, we expect private consumption growth, and broader GDP growth, to bounce back in Q1-2020.

Previous: 1.4% (Year-over-Year) Consensus: 1.4%

Canada Employment • Friday

Canada’s November employment report was a miss nearly across the board, as employment fell 71,200 with declines in full-time and part-time positions. The jobless rate unexpectedly jumped to 5.9%, although wage growth held steady at 4.4% year over year. The report followed a fairly strong performance from Canada’s labor market over most of the earlier part of the year, with strong gains in full-time jobs and a robust increase in wage growth.

Given that prior outperformance, next Friday’s release of employment data for December will be all the more important in discerning whether November was an anomaly or the beginning of a more sustained slowdown in Canadian hiring activity. In our view, it is a bit hard to square the November report with other Canadian indicators, and we are of the view that it was not the beginning of a sharp slowdown in economic growth in Canada.

Previous: -71.2K (Net Change in Employment) Consensus: 31.7K

Mexico CPI • Thursday

Mexico’s economy has essentially stagnated over the past two years or so, struggling under the weight of sky-high real interest rates and, more recently, sharply slower growth across most of the world’s major economies. Restrictive monetary policy and weaker GDP growth conspired to bring down inflation in 2018, but more recently, core CPI inflation has risen, rather than slowed. To be sure, the acceleration has not been unruly, and core inflation remains close to the central bank’s 3% target. However, the fact that core inflation has not eased more may be one reason why the central bank has been hesitant to cut interest rates more aggressively and provide more policy support to a domestic economy that has stagnated for two years. The central bank has cut rates at each of its last four meetings, but only by 25 bps each time, and thus real interest rates remain close to 4%. More aggressive rate cuts seem unlikely until core inflation shows more concrete signs of slowing.

Previous: 3.0% (Year-over-Year)

Point of View

Interest Rate Watch

FOMC Slightly More Hawkish in 2020

The new year will see some changes on the Federal Open Market Committee (FOMC). When fully staffed, the FOMC contains 19 members, 12 of which are voting members. In “normal times” there are seven Governors of the Federal Reserve System. However, the Federal Reserve Board, which sits in Washington, DC has not been fully staffed since August 2013. Presently, there are five Governors, and all of these Governors vote at every FOMC meeting.

The president of the Federal Reserve Bank of New York votes at every FOMC meeting as well. The remaining four voting positions are rotated on a set schedule every year among the other 11 presidents of the Federal Reserve Banks. Last year’s voters from the Boston, Chicago, Kansas City and St. Louis Federal Reserve Banks have been replaced this year by the presidents of the Cleveland, Dallas, Minneapolis and Philadelphia Feds.

Eric Rosengren (Boston) and Esther George (Kansas City) are “hawks.” Indeed, both presidents dissented each time the FOMC cut rates at the July, September and October FOMC meetings. On the other hand, Charles Evans (Chicago) and James Bullard (St. Louis) are “doves.” The two “hawks” from last year have been replaced by Loretta Mester (Cleveland) and Patrick Harker (Philadelphia), who also tend to the hawkish side of the spectrum. Neel Kashkari (Minneapolis) is very dovish, but Robert Kaplan tends to be middle-of-the-road in terms of his policy views. Therefore, the change in voting members tilts the FOMC in a slightly more hawkish direction this year.

That said, the committee likely will not be raising rates anytime soon. As we noted in a recent report, we look for the FOMC to keep rates on hold through the end of 2021. Although we acknowledge that the committee could conceivably start to tighten policy again in 2020, we believe that GDP growth would need to be materially stronger and/or inflation significantly higher than Fed policymakers currently expect. Most market participants also seem to agree that the committee will be on hold for the foreseeable future. Market pricing indicates that the probability of a rate hike at each of the FOMC meetings in 2020 is less than 5%.

Credit Market Insights

Swedish Debt Underperforming

In 2019, the global bond market was relatively strong, but Swedish debt underperformed its euro-area peers. The Bloomberg Barclays Treasury indexes showed that Swedish bonds gained just 2.4% compared to the euro-area at 7.2%, and significantly lagged Italy at 10.6%.

Over the past month, Sweden’s bonds fell leading up to the Riksbank’s December policy meeting in which the Riksbank raised its repo rate 25 bps to 0.00%, ending several years of negative interest rates. The market had largely priced in a Riksbank hike, so the krona’s moves as well as Sweden’s fixed income market moves following the announcement were fairly muted. The central bank’s decision to tighten policy defied the overall trend of easing policy, which may have contributed to some of the limitations for Swedish debt to gain. Meanwhile, Swedish debt has also struggled against its peers such as Italy and Germany, as both countries benefitted from ECB policy easing as well as other easing measures such as the resumption of its asset purchase program. However, given that Sweden is not part of the Eurozone, it did not reap the same gains.

From a currency perspective, the krona has also lagged its peers, and is 2019’s worst performer among G10 currencies as political uncertainty and slower global growth has kept the krona on the defensive. With the Riksbank rate hike now past, it may be difficult for the krona to gain any further traction going into the new year.

Topic of the Week

Budget Package Delivers the Presents Early

During the week of Dec. 16, Congress passed legislation to fund the federal government through FY 2020 and avoid a repeat of last year’s government shutdown. Since the fiscal year began on Oct. 1, the government had been operating under a series of continuing resolutions. Policymakers agreed on top-line spending levels back in July, but since then had been struggling to pass legislation that appropriates the money to the various government agencies and programs. The December budget package appropriates the money and formally authorizes the government to spend the full amount agreed to over the summer. As we wrote in July, the spending increase in FY 2020 is much smaller than what was seen in FY 2018/2019, and as such the incremental impact on real GDP growth is likely to be smaller. We expect federal government consumption and investment to add roughly 0.1-0.2 percentage points to headline GDP growth over the next few quarters (top chart).

The spending package went well beyond just appropriating the top-line spending levels. Perhaps most relevant to the macro outlook was the permanent repeal of three key Affordable Care Act (ACA) taxes: an excise tax on medical devices, an excise tax on high cost employer-sponsored health insurance (often referred to as the “Cadillac Tax”) and an annual fee imposed on health insurance providers. All three of these taxes were originally passed as part of the ACA, but in the ensuing years their implementation was repeatedly delayed. This legislation permanently repeals them, to the tune of $373 billion in lost revenues over the next decade (bottom chart).

Since these taxes are not currently in effect, however, it is important to remember that this “lost” revenue is only lost relative to current law, and not current policy. Thus, the near term macro impact from this repeal on the federal budget deficit and the $21 trillion U.S. economy is likely to be negligible. Longer-term federal budget deficit projections, however, will now likely look even bigger than previously projected.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals