Australian Dollar trades mildly lower today as Asian stocks outside China are paring gains. Also, as coronavirus virus cases surged again in Victoria state, Melbourne is back in lockdown. Meanwhile, RBA stands pat as widely expected and provide little inspirations. As for now, commodity currencies are also weak while Dollar and Sterling are the stronger ones.

Technically, despite yesterday’s selloff, Dollar is generally holding above near term support level. Those levels include 1.1348 resistance in EUR/USD, 1.2542 resistance in GBP/USD, 0.7064 resistance in AUD/USD. 1.3485 support in USD/CAD and 106.79 support in USD/JPY. We’ll see if Dollar could strike a comeback today.

In Asia, Nikkei closed down -0.44%. Hong Kong HSI dropped -0.57%. China Shanghai SSE is up 1.45%. Singapore Strait Times is down -0.51%. Japan 10-year JGB yield is down -0.0007 at 0.038. Overnight, DOW rose 1.78%. S&P 500 rose 1.59%. NASDAQ rose 2.21% to 10433.65, another record high. 10-year yield rose 0.015 to 0.684.

RBA stands pat and pledged not to raise interest rate until progress is made

RBA kept monetary policy unchanged as widely expected. The cash rate is held at 0.25% and target of 3-year AGS yield at 0.25% too. The central bank also pledged to maintain the accommodative approach for “as long as it is required”. Also, “the Board will not increase the cash rate target until progress is being made towards full employment and it is confident that inflation will be sustainably within the 2–3 per cent target band.”

RBA also said the employment conditions have “stabilised” recently and the economic downturn has been “less severe than earlier expected”. However, the “nature and speed” of economic recovery remains “highly uncertain”. Uncertainty is also ‘affecting consumption and investment plans”. The pandemic is prompting many firms to “reconsider their business models”.

Australia AiG services dropped back slightly to 31.5, employment shrank further

Australia AiG Performance of Services Index dropped -0.1 to 31.5 in June. The reading indicates “another serious contraction in activity” at a pace similar to May. That’s also the second lowest record reading next to April’s. Looking at some details, all indicates remains firmly below series average despite lockdown easing. In particular, employment dropped a further -4.3 pts to 30.9.

New Zealand NZIER business confidence improved, but stays low on pre-election and pandemic uncertainty

NZIER Quarterly Survey of Business Opinion showed a net 37% of businesses reported decline in activity during Q2. That’s the worst level since March 2009 due to tight trading restrictions under Alert Level 4 lockdown. Also, a net 25% of businesses expect weaker demand in Q3.

There was a slight improvement in headline business confidence, from -70 to -63. But the reading suggests that businesses remain pessimistic over the coming months, and they could be holding off on major spending decisions. Pre-election uncertainty is compounded by how the coronavirus pandemic will play out.

Japan labor cash earnings dropped -2.1%, household depending dropped record -16.2%

Japan labor cash earnings dropped -2.1% yoy in May, well below expectation of -1.1% yoy. That’s also the steepest decline since the -2.8% fall recorded back in June 2015. A labor ministry official was quoted by Reuters saying that “the impact from the coronavirus led to a reduction in overtime pay which caused real wages to fall a lot.”

Household spending dropped -16.2% yoy, also much worse than expectation of -12.2% yoy. That’s a record decline since comparable data first became available in January 2001. It also followed a prior record of -11.1% yoy decline reported a month ago in April.

Despite the poor data, BoJ could likely keep at economic assessment unchanged in the post statement meeting next week. It’s believed that the economy had already hit the bottom in Q2, like many other countries in the world. The question now is on the pace and sustainability of recovery.

Looking ahead

Germany industrial production, France trade balance, Italy retail sales and Swiss foreign currency reserves will be featured in European session. Canada will release Ivey PMI.

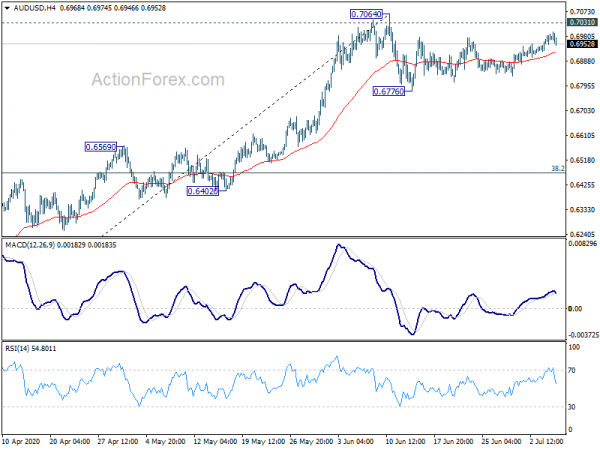

AUD/USD Daily Report

Daily Pivots: (S1) 0.6939; (P) 0.6963; (R1) 0.6998; More…

AUD/USD’s recovery lost momentum again ahead of 0.7064 high. Intraday bias remains neutral first. At this point, we’d still expect correction from 0.7064 to extend with another falling leg. On the downside, break of 0.6776 will turn bias to the downside for 38.2% retracement of 0.5506 to 0.7064 at 0.6469. Nevertheless, sustained break of 0.7064 will resume whole rise from 0.5506 instead.

In the bigger picture, rebound from 0.5506 medium term bottom could be correcting whole long term down trend from 1.1079 (2011 high). Further rally would be seen to 55 month EMA (now at 0.7310). This will remain the preferred case as long as it stays above 55 week EMA (now at 0.6734). Sustained trading below 55 week EMA will turn focus back to 0.5506 low instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Jun | 31.5 | 31.6 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y May | -2.10% | -1.10% | -0.70% | |

| 23:30 | JPY | Overall Household Spending Y/Y May | -16.20% | -12.20% | -11.10% | |

| 4:30 | AUD | RBA Rate Decision | 0.25% | 0.25% | 0.25% | |

| 4:30 | AUD | RBA Rate Statement | ||||

| 5:00 | JPY | Leading Economic Index May P | 79.2 | 79.5 | 77.7 | |

| 6:00 | EUR | Germany Industrial Production M/M May | 7.80% | 10.00% | -17.90% | -17.50% |

| 6:45 | EUR | France Trade Balance (EUR) May | -4.5B | -5.0B | ||

| 7:00 | CHF | Foreign Currency Reserves (CHF) Jun | 816B | |||

| 8:00 | Italy | Italy Retail Sales M/M May | 15.00% | -10.50% | ||

| 15:00 | CAD | Ivey PMI Jun | 50.2 | 39.1 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals