The latest CPI numbers out of the US will hit the markets at 12:30 GMT Friday, and forecasts suggest inflation picked up some steam. If that is the case, then market expectations for any Fed easing at next week’s policy meeting might fade entirely, helping euro/dollar to extend its correction lower – especially now that the ECB is actively talking down the euro. In the bigger picture, whether the stock market sell-off continues will be crucial too.

ECB: The dollar’s unlikely hero

The world’s reserve currency had a tough summer. It fell for four straight months, as the euphoric atmosphere in the markets suppressed demand for defensive plays. Meanwhile, the Fed went on the offensive. The central bank said it will allow the US economy to ‘run hot’, meaning that it will not lift a finger to restrain inflation even if it exceeds its 2% target.

The signal was that interest rates will stay low for a very long time and that the Fed will need to see inflation closer to 2.5% before it even considers raising them again, adding to the dollar’s pain.

But then September came along, and the dollar got its feet under it again, with a little help from the European Central Bank (ECB). The ECB fired a verbal barrage to shoot the high-flying euro down, indicating that if it continues to appreciate it could hold back the economic recovery. The result was a weaker euro, which by extension lifted the dollar, as for every loser there must be a winner in FX.

The recent stock market selloff likely supported the haven-like greenback as well, alongside some worrisome Brexit headlines that pushed sterling lower.

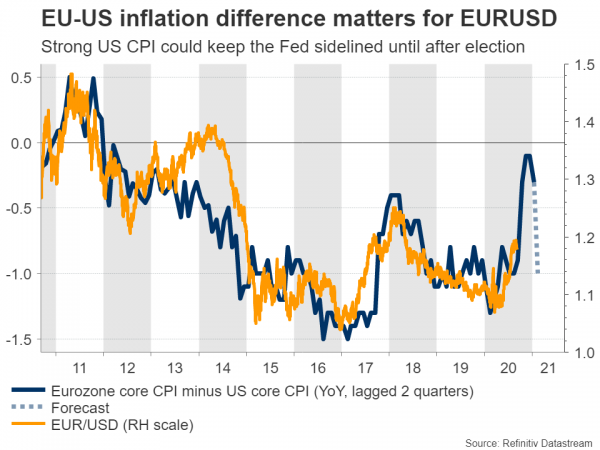

CPI data might keep Fed on a leash

The Federal Reserve meets next week, and investors will be looking for clues on whether the Fed will take any further action to push inflation higher. That is why the upcoming CPI data are so important. If inflation is indeed as resilient as forecasts suggest, that would diminish the odds for any more immediate easing measures.

In August, the consumer price index (CPI) is expected to clock in at 1.2% in yearly terms, an acceleration from the 1.0% previously. The core rate that excludes the effects of volatile items like fresh food and gasoline is expected to hold steady at 1.6%. That is not a bad reading in the middle of a recession, which is by nature a deflationary event.

If the actual prints meet or exceed expectations, this might give the Fed the green light to sit back until the US election has passed, which would argue for a spike higher in the dollar.

The bigger picture

Looking beyond this week, signs are accumulating that the dollar’s recovery may still have room to run. The notion that the Eurozone will outperform the US has been the main driving force behind the euro’s incredible gains, but that view is now coming into doubt as new coronavirus cases spike in countries like Spain and France, while European activity indicators are losing steam.

At the same time, the ECB is actively trying to hold the euro down and sterling is being tormented by Brexit fears once more, so the alternatives to the dollar are suddenly not as attractive.

These would argue in favor of the correction to continue, though a lot will also depend on how global risk sentiment evolves. If stock markets climb back to all-time highs for example, that might overshadow everything else and push the dollar back down.

Taking a technical look at euro/dollar, if the bears manage to pierce below the 1.1760 zone, their next target might be the 1.1710 region.

On the flipside, if the latest rebound continues, resistance may be found near the 1.1880 area, with an upside break opening the door for 1.1915.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals