As the COVID-19 vaccine is released, life will revert to the “old normal”. However, that doesn’t necessarily mean it will be good for the markets!

It has been over a year since the first cases of the COVID-19 were diagnosed in Wuhan, China. As a result of the virus, we have seen an unfathomable global shutdown in Q2, followed by a record-setting return to growth in Q3 as the summer months arrived. Q4 resulted in second and third waves. In November, results of Phase 3 vaccine studies began to trickle in and by the end of the year, frontline workers and those most in need were already receiving the first doses.

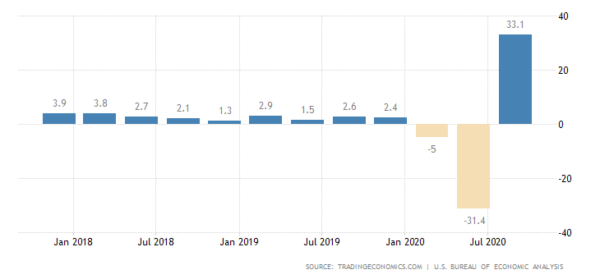

US Annualized GDP Growth Rate:

Source: Trading Economics, BLS

The first few months of 2021 will likely continue in the same manner as 2020 ended:

- threats of global lockdowns and restrictions as the virus lingers

- depressed economic data, primarily in services

- additional fiscal and monetary support from governments and central banks around the world

As we move into Q2 and the vaccines become more widely available, things should begin to return to the “old normal.” However, although a return to the “old normal” may be better for daily life, it may not be so great for the markets. As we move through 2021, below are some markets to watch as the vaccine is dispersed:

Economic Data

As we progress through the year, employment should pick up and initial claims should decrease. As people return to work after being cooped up for the better part of a year, PMIs should continue to recover, especially in the services industries. Industries such as food services, cruise lines, airlines, and hospitality could outperform. The “stay at home” industries, such as technology (which includes FAANG stocks) may underperform. GDP should continue to rise – however, the growth rate may begin to level off towards the end of the year. Housing should stay strong on the back of a demographic tailwind and millennials seeking to “beat the rush” in anticipation of higher interest rates.

US Dollar

With a vaccine on the way and more people returning to work, there will be less need for fiscal and monetary stimulus; however many central banks have indicated that they will keep monetary policy accommodative through 2021. The US Dollar could remain under pressure through the first half of the year but may rebound heading into Q3 and Q4 as the FOMC may hint at raising interest rates if inflation picks up heading into in 2022.

To put it simply, better economic data equals less stimulus. Less stimulus means less US Dollars in the system. Less US Dollars (plus higher demand for products and services) equals higher price.

On a monthly timeframe, the DXY has broken below the upward sloping trendline from September 2011. If that level breaks, watch for the 50% retracement level from the February 2008 lows to the January 2017 highs as the next support level, near 87.10. Below there was the 50% retracement level near 87.26 and the horizontal support near 84.60.

Source: Tradingview, GAIN Capital

Stocks

The Dow Jones Industrial Average traded above 30,000 for the first time ever in November. The S&P 500 and NASDAQ are near all-time highs. As the vaccine is introduced to the world population and lockdowns are lifted, we should see a rotation out of “stay at home” stocks and a return to value stocks. Keep in mind however that as the Federal Reserve and other central banks begin to worry less about stimulus and more about inflation in Q3 or Q4, stocks might not be as excited and may begin to turn lower. In the Dow, 32,700 is the 127.2% Fibonacci extension from the highs during the week of February 10th to the lows the week of March 23rd:

Source: Tradingview, GAIN Capital

2-Year Yields

With the introduction of a vaccine to the general public in the first half of the year, 2-year yields should remain between 0%-0.25%. If the word “inflation” enters the FOMC’s vocabulary during this year, rates should turn higher, which may be dramatic as the market tries to price in inflation expectations.

Source: Tradingview, GAIN Capital

Crude Oil

As more and more people around the world receive the vaccine, demand for manufacturing will increase. Travel will begin to return to normal and airlines and cruise ships will return to normal operations. The increase in demand could serve as a tailwind for the price for oil. Watch for WTI to continue to move higher as a vaccine is rolled out, possibly testing the January 2020 highs of $65.66.

Source: Tradingview, GAIN Capital

As pharmaceutical companies release more and more of the COVID-19 vaccine, economies should begin to recover, and life will revert to the “old normal”. However, that doesn’t necessarily mean it will be good for the markets as central banks may begin using the words “inflation” and “less stimulus”.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals