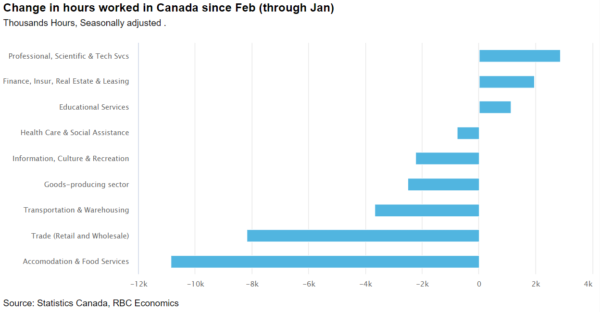

Next week will be a quiet week for economic data releases and much of the focus will be centered on reopening plans. Steadily declining COVID case counts across most regions of Canada have already resulted in some easing in containment measures and we expect this will continue. Even as some parts of the economy reopen, we expect restrictions will stay in place on activity in the high-contact hospitality sector as long as virus threat remains. All said, the economic backdrop will look better in February than in January. The impact of the latest round of containment measures has been narrowly based to the ‘high-contact’ hospitality sector, along with ‘non-essential’ retailers. Outside of those hard-hit sectors, labour markets have generally continued to improve. Even with the whopping 213k drop in employment reported in January, total hours worked increased by almost a percent. That reinforced that overall economic activity has held up much better than during spring 2020 lockdowns, potentially even leaving upside risk to our forecast for a flat Q1 GDP growth reading.

News on vaccine distribution delays will also be watched closely – beyond the very near-term, the single most important determinant for the rest of this year will be the speed of vaccine roll-out, and effectiveness of those vaccines at curbing the pandemic. The government planned for the administration of roughly 400k doses per week by the end of February, but disruptions to distribution out of production facilities in Europe have delayed deliveries. Government officials have been sticking with guidance that 6 million doses will be available by the end of March.

Week ahead data watch:

- We look to see US Headline CPI post another increase in January albeit holding well below the Fed’s target. This number will likely trend higher as it will benefit from a lower base effect that will show up in the spring.

- COVID-19 case counts and vaccine deployment will be watched closely alongside any removal of containment measures.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals