New Zealand Dollar opens the week higher after ratings upgrade by S&P. The Kiwi would now look into RBNZ’s comments on the economy and new economic projections featured later in that week. Elsewhere, overall risk-on sentiments continue to support commodity currencies and Sterling. On the other hand, Yen and Swiss Franc are trading generally lower, followed by Dollar and Euro.

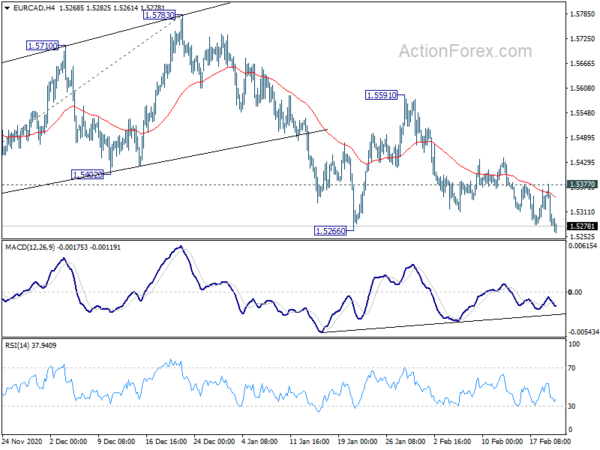

Technically, USD/CAD’s breach of 1.2588 low suggests that down trend is resuming. But there is no follow through selling so far. Similarly, EUR/CAD also breached 1.5266 low, suggesting resumption of fall from 1.5978. Such decline could target 100% projection of 1.5970 to 1.5313 from 1.5783 at 1.5118. But of course, EUR/CAD has to build up some downside momentum below 1.5266 first. Or, rebound from current level, followed by break of 1.5377 minor resistance, will extend recent sideway trading instead.

In Asia, currently, Nikkei is up 0.54%. Hong Kong HSI is up 0.46%. China Shanghai SSE is down -0.06%. Singapore Strait Times is up 0.26%. Japan 10-year JGB yield is up 0.0082 at 0.114.

Fitch affirms Australia rating at AAA with negative outlook

Fitch Ratings affirmed Australia’s Long-Term Foreign-Currency Issuer Default Rating at “AAA” with a negative outlook. The rating reflects the country’s “strong institutions and effective policy framework, which supported nearly three decades of economic growth prior to the coronavirus pandemic and helped limit the severity of the current shock”

But the negative outlook reflects “uncertainty around the medium-term debt trajectory following the significant rise in public debt/GDP caused by the response to the pandemic.”

Fitch estimated that GDP contracted by -2.8% in 2020, versus “AAA” median of -3.8%. Economy is forecast to growth 3.8% in 2021 and 2.7% in 2022. It expects closure of international borders to persist until late-2021, which “dampened inward migration”. Trade tension with China “have not had a significant macroeconomic effect”, but remains a medium term risk.

S&P upgrades New Zealand rating back to AA+/AAA

S&P raised New Zealand’s foreign and local currency government debt rating by a notch to AA+ and AAA, up from AA and AA+ respectively. The ratings are back to a level last seen in 2009. A “stable” outlook was attached to the new ratings.

“New Zealand is recovering quicker than most advanced economies after the Covid-19 pandemic and subsequent government lockdown delivered a severe economic and fiscal shock to the country,” S&P said. “While downside risks persist, such as another outbreak, we expect New Zealand’s fiscal indicators to recover during the next few years.”

“This provides us with better clarity over the extent of the pandemic’s damage to the government’s balance sheet,” it said in a statement,” it said, “We now believe that the government’s credit metrics can withstand potential damage from negative shocks to the economy, including a possible weakening of the real estate market”.

NZD/USD resumes up trend, long term resistance at 0.75

NZD/USD’s up trend resumes by breaking through 0.7314 resistance today and hits as high as 0.7337 so far. From a near term perspective, current rise from 0.5469 should target 61.8% projection of 0.6589 to 0.7314 from 0.7156 at 0.7604 next.

However, a key cluster resistance at 0.7557, 61.8% retracement of 0.8835 (2014 high) to 0.5469 (2020 low) at 0.7549, comes just before above mentioned 0.7604 projection target. Additionally, RBNZ statement poses a slight risk to the Kiwi, in the sense that it may want to talk down the strong exchange rate.

So we’d pay close attention to the momentum of next move. But in any case, outlook will stay bullish as long as 0.7156 support holds, even in case of deep retreat.

RBNZ and Fed Powell in focus for the week

RBNZ is widely expected to keep monetary policy unchanged this week. OCR will be held at 0.25%, while the LSAP program will be kept at NZD 100B. After some encouraging economic data, RBNZ could sound more upbeat in the statement, as well as economic projections. Negative rate is more likely ruled out for not. Nevertheless, the central might also want to refrain from saying anything that boost Kiwi’s exchange rate. The question is on how RBNZ would strike that balance.

Previews on RBNZ:

Fed Chair Jerome Powell’s testimony will be another major focuses. Markets would look for his reaffirmation that it’s not time to even talk about stimulus exit. Additionally, he might dismiss the near term risk of inflationary pressure as temporary. Rather, Fed would stay with the current highly accommodative stance, and look through near term fluctuation in inflation data, to medium term outlook.

Here are some highlights for the week:

- Monday: Germany Ifo business climate; US leading indicator.

- Tuesday: New Zealand retail sales; Australia goods trade balance; UK employment; Swiss PPI; Eurozone CPI final; US house price indices, consumer confidence.

- Wednesday: RBNZ rate decision; Australia wage price index; German GDP final; US new home sales.

- Thursday: New Zealand ANZ business confidence; Australia private capital expenditure; Germany Gfk consumer climate; Eurozone M3 money supply; US GDP revision, durable goods orders, jobless claims, pending home sales.

- Friday; New Zealand trade balance; Australia private sector credit; Japan Tokyo CPI, industrial production, retail sales, housing starts; Swiss GDP; Germany import price; France GDP; Swiss KOF economic barometer; Canada IPPI, RMPI; US personal income and spending, goods trade balance, wholesale inventories, Chicago PMI.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3959; (P) 1.3998; (R1) 1.4043; More….

Intraday bias in GBP/USD remains on the upside at this point. Current up trend from 1.1409 is in progress for 1.4376 long term resistance next. On the downside, break of 1.3950 minor support will turn intraday bias neutral, and bring consolidations, before staging another rally.

In the bigger picture, rise from 1.1409 medium term bottom is in progress. Further rally would be seen to 1.4376 resistance and above. Decisive break there will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. On the downside, break of 1.3482 resistance turned support is needed to be first indication of completion of the rise. Otherwise, outlook will stay cautiously bullish even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Jan | -0.50% | -0.40% | -0.40% | -0.30% |

| 9:00 | EUR | Germany IFO Business Climate Feb | 90.5 | 90.1 | ||

| 9:00 | EUR | Germany IFO Current Assessment Feb | 88.9 | 89.2 | ||

| 9:00 | EUR | Germany IFO Expectations Feb | 91.9 | 91.1 | ||

| 15:00 | USD | Leading Index Jan | 0.30% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals