Swiss Franc was a focus in earlier European session as it suffered brief but deep selloff. Though, it somewhat found some footing quickly, even though it’s still the second weakest for today so far. Yen is underperforming again on strong major global benchmark yields. Dollar and Canadian Dollar are the next weakest even though Euro is not far behind. Kiwi and Aussie are trading as the strongest ones for the moment.

Technically, EUR/CHF’s break of 1.0890 resistance suggests that larger rebound from 1.0503 is resuming. Sustained trading above 1.0915 will confirm and target 61.8% projection of 1.0503 to 1.0915 from 1.0737 at 1.0992. Though, to confirm overall weakness in the Swiss Franc, we’d like to see at least the break of 0.9044 resistance in USD/CHF, and preferably the break of 116.20 support in CHF/JPY too.

In bond markets, US 10-year yield is up 0.0375 at 1.377. German 10-year yield is up 0.003 at -0.302. UK 10-year gilt yield is up 0.020 at 0.720. Japan 10-year JGB yield closed up 0.0140 at 0.120. In stocks, FTSE is down -0.69%. DAC is down -0.66%. CAC is down -0.48%. In Asia, Nikkei rose 0.46%. Hong Kong HSI dropped -1.06%. China Shanghai SSE dropped -1.45%> Singapore Strait Times rose 0.02%.

German Ifo business climate rose to 92.4, manufacturing at best since 2018

Germany Ifo Business Climate rose to 92.4 in February, up from 90.3, above expectation of 90.5. Current Assessment index rose to 90.6, up from 89.2, above expectation of 88.9. Expectations index rose to 94.2, up from 91.5, above expectation of 91.9.

Looking at some details, manufacturing index rose from 9.1 to 16.1, highest since November 2018. Services rose from -4.4 to -2.2. Trade rose from -17.2 to -14.6. Construction rose from -4.9 to -3.6.

Clemens Fuest, President of the ifo Institute, said “the German economy is proving robust despite the lockdown, especially thanks to strength in industry.”

Fitch affirms Australia rating at AAA with negative outlook

Fitch Ratings affirmed Australia’s Long-Term Foreign-Currency Issuer Default Rating at “AAA” with a negative outlook. The rating reflects the country’s “strong institutions and effective policy framework, which supported nearly three decades of economic growth prior to the coronavirus pandemic and helped limit the severity of the current shock”

But the negative outlook reflects “uncertainty around the medium-term debt trajectory following the significant rise in public debt/GDP caused by the response to the pandemic.”

Fitch estimated that GDP contracted by -2.8% in 2020, versus “AAA” median of -3.8%. Economy is forecast to growth 3.8% in 2021 and 2.7% in 2022. It expects closure of international borders to persist until late-2021, which “dampened inward migration”. Trade tension with China “have not had a significant macroeconomic effect”, but remains a medium term risk.

S&P upgrades New Zealand rating back to AA+/AAA

S&P raised New Zealand’s foreign and local currency government debt rating by a notch to AA+ and AAA, up from AA and AA+ respectively. The ratings are back to a level last seen in 2009. A “stable” outlook was attached to the new ratings.

“New Zealand is recovering quicker than most advanced economies after the Covid-19 pandemic and subsequent government lockdown delivered a severe economic and fiscal shock to the country,” S&P said. “While downside risks persist, such as another outbreak, we expect New Zealand’s fiscal indicators to recover during the next few years.”

“This provides us with better clarity over the extent of the pandemic’s damage to the government’s balance sheet,” it said in a statement,” it said, “We now believe that the government’s credit metrics can withstand potential damage from negative shocks to the economy, including a possible weakening of the real estate market”.

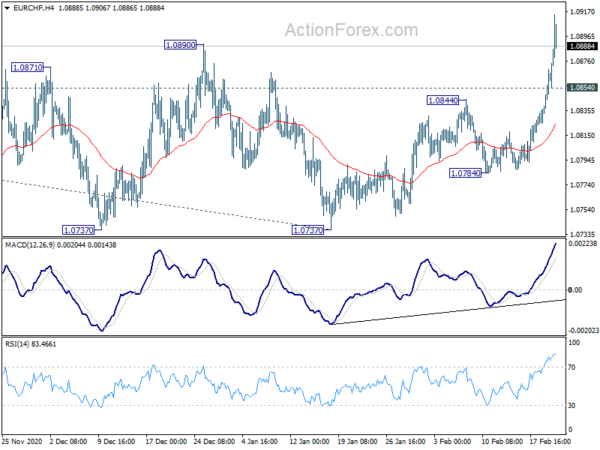

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0841; (P) 1.0856; (R1) 1.0879; More….

EUR/CHF’s strong break of 1.0890 resistance argues that consolidation from 0.915 has completed at 1.0737. Larger rebound from 1.0503 is possibly resuming. Intraday bias stays on the upside. Firm break of 1.0915 will confirm and target 61.8% projection of 1.0503 to 1.0915 from 1.0737 at 1.0992. On the downside, below 1.0854 minor support will turn intraday bias neutral again for some more consolidations.

In the bigger picture, price actions from 1.0503 are still seen as a consolidation pattern. With 1.1059 cluster resistance (38.2% retracement of 1.2004 to 1.0503 at 1.1076) intact, the down trend from 1.2004 (2018 high) would still extend through 1.0503 low at a later stage. However, sustained break of 1.1059/76 will argue that rise from 1.0503 is starting a new up trend and would target 61.8% retracement at 1.1431 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Jan | -0.50% | -0.40% | -0.40% | -0.30% |

| 9:00 | EUR | Germany IFO Business Climate Feb | 92.4 | 90.5 | 90.1 | 90.3 |

| 9:00 | EUR | Germany IFO Current Assessment Feb | 90.6 | 88.9 | 89.2 | |

| 9:00 | EUR | Germany IFO Expectations Feb | 94.2 | 91.9 | 91.1 | 91.5 |

| 15:00 | USD | Leading Index Jan | 0.30% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals