Selling focus appears to be turning to Yen as markets enter into US session. Swiss Franc remains weak but the decline is slowing slightly. Dollar and Euro are also soft, but both are supported by buying against Yen and Franc. On the other hand, commodity currencies remain the strongest ones for today as led by New Zealand Dollar. Canadian Dollar follows as second, with help from mild strength in oil price.

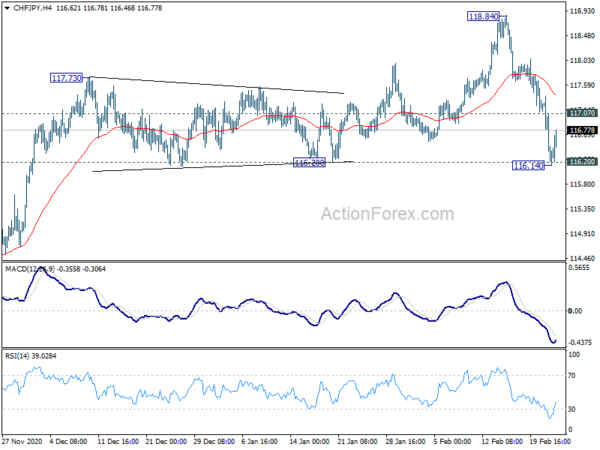

Technically, 106.21 resistance in USD/JPY would now be an immediate focus with today’s strong rally. Break will resume whole rise from 102.58, for 108.22 fibonacci level. CHF/JPY appears to be drawing support from 116.20. Break of 117.07 will confirm defending the support level and bring stronger rebound. That would also confirm that the tide has turned against the Yen, which might help USD/JPY break through 106.21.

In Europe, currently, FTSE is up 0.21%. DAX is up 0.76%, CAC is up 0.06%. German 10-year yield is up 0.012 at -0.302. Earlier in Asia, Nikkei dropped -1.61%. Hong Kong HSI dropped -2.99%. China Shanghai SSE dropped -1.99%. Singapore Strait Times rose 1.17%. Japan 10-year JGB yield rose 0.0031 to 0.123.

Germany GDP finalized at 0.3% qoq in Q4, -3.7% yoy

Germany Q4 GDP growth was finalized at 0.3% qoq, revised up from 0.1% qoq. Over the year, on price-adjusted term, GDP dropped -2.7% yoy. In Price and calendar-adjusted terms, GDP dropped -3.7% yoy.

Destatis said, “in the fourth quarter, however, the recovery process slowed due to the second coronavirus wave and another lockdown imposed at the end of the year.”

BoJ Kuroda: Various tools including ETF purchases will be target of March policy framework review

BoJ Governor Haruhiko Kuroda told the parliament today that “the BOJ’s various tools, including its ETF buying, will be the target of the March review. We’ll examine how our tools are affecting markets and look at what we can do better.” He added that government bond buying has already slowed substantially as markets are calm. Average duration of the bond holdings also remained stable a around seven years.

Separately, former BoJ deputy governor Hirohide Yamaguchi told Reuters that BoJ’s review is “unlikely” to come up with “an outcome that has a substantial impact on the economy and markets. “The review will probably be just a show of gesture that it’s doing ‘something’ to address the cost,” said Yamaguchi.

“It’s impossible for the BOJ to guide public perceptions at its will,” Yamaguchi added. “It’s time now for the BOJ to conduct a ‘genuine’ policy review and use the findings to modify its policy framework.”

RBNZ keeps policy unchanged, prolonged monetary stimulus needed

RBNZ left monetary policy unchanged today as widely expected. OCR is held at 0.25%, Large Scale Asset Purchase Programme at up to NZD 100B and Funding for lending program unchanged. Current monetary policy setting were seen as “appropriate” to achieve the central bank’s inflation and employment remit. But a “prolonged period of time” is needed before meeting the conditions of removing monetary stimulus.

In the Monetary Policy Statement, RBNZ said the economic rebound has been “stronger than expected”. But domestic recovery “has been uneven” while outlook is “highly uncertain”. “Significant stimulus is still required” and “interest rates are assumed to remain at historically low levels for an extended period.”

Suggested readings on RBNZ:

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 104.98; (P) 105.21; (R1) 105.49; More..

Focus is now on 106.21 resistance with today’s strong rally. Firm break there will resume rise from 102.58, to 61.8% retracement of 111.71 to 102.58 at 108.22. Rejection by 106.21 will bring more consolidations but further rally will remain in favor as long as 104.91 support holds. However, break of 104.91 should now indicate completion of the rise from 102.58 and turn near term outlook bearish.

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016), and there is no clear indication of trend reversal yet. Though, sustained trading above 55 week EMA (now at 105.84) will be the first sign of reversal and turn focus to channel resistance (now at 110.15).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Wage Price Index Q/Q Q4 | 0.60% | 0.20% | 0.10% | |

| 0:30 | AUD | Construction Work Done Q4 | -0.90% | 1.10% | -2.60% | -1.80% |

| 1:00 | NZD | RBNZ Interest Rate Decision | 0.25% | 0.25% | 0.25% | |

| 7:00 | EUR | Germany GDP Q/Q Q4 F | 0.30% | 0.10% | 0.10% | |

| 9:00 | CHF | ZEW Expectations Feb | 55.5 | 43.2 | ||

| 15:00 | USD | New Home Sales M/M Jan | 859K | 842K | ||

| 15:30 | USD | Crude Oil Inventories | -6.5M | -7.3M |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals