The European Central Bank (ECB) will wrap up its policy meeting at 12:45 GMT Thursday. Some senior policymakers have been vocal about fighting the rise in bond yields, but it is probably too early for that. If the ECB takes no immediate action, the euro could gain on the decision, though the bigger picture is negative.

ECB thinks this is a US problem

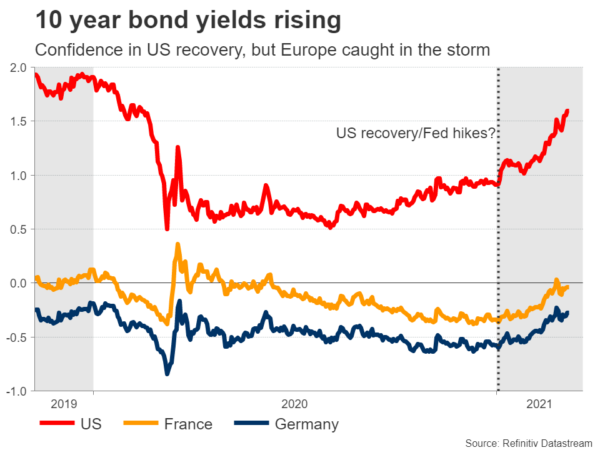

Rising bond yields can be both a blessing and a curse. On the bright side, they signal that investors are becoming more confident in the recovery, bringing forward the expected timing of rate increases by central banks. Unfortunately, rising yields also raise the cost of borrowing in the economy, which can hold back the recovery if the moves are excessive.

From the ECB’s point of view, this is mostly an American story that is spilling over into the European bond market. The swift pace of US vaccinations and the barrage of federal spending is leading investors to price in Fed rate hikes by late 2022-early 2023, pushing US yields higher and dragging European yields higher in the process.

However, the euro area economy is not healing. Lockdowns have been extended in most nations, vaccinations have been painfully slow, and government spending hasn’t been impressive. As a result, some senior ECB officials have warned that this spike in yields is unwarranted and that it should be resisted.

Just talk, no action?

That said, it is probably too early for the ECB to take action. While some officials have called for an immediate acceleration of QE purchases to push yields back down, several others have downplayed the need for immediate action, suggesting that they can manage this risk simply through verbal intervention. Threatening markets with action may be enough for now.

There’s also an argument for not overreacting to every market move, especially since yields are still near historic lows. If the move persists and threatens borrowing or economic conditions, then the ECB will hit the panic button.

If the central bank falls short of signalling action and simply resorts to words, that could give markets the green light to push yields and by extension the euro higher. Taking a technical look at euro/dollar, initial resistance to advances may come from the 1.1950 zone, a break of which would turn the focus to 1.1990.

But overall euro outlook bleak

In the bigger picture though, even if the euro rebounds this week, the overall outlook still looks negative. The ECB’s pain threshold for higher yields is quite low, and it could very well take action to fight this move if it persists. In contrast, the Fed will only intervene if things really get out of control.

This implies that interest rate differentials between Europe and America could widen further, weighing down on euro/dollar. It is not just a short-term story either. A booming US economy thanks to all the federal spending implies that the Fed will almost certainly normalize policy before the ECB does, first by scaling back QE and ultimately by raising rates.

We might be in a situation by early 2022 where the Fed is tapering its QE purchases, but the ECB is extending them. Markets could begin to price in this divergence in monetary policies much earlier. Indeed, positioning on the euro by leveraged speculators is still stretched long according to the latest CFTC data, so there’s a lot of scope for further downside as those bullish bets are unwound.

In case euro/dollar resumes its recent decline, the first target for sellers may be the recent low of 1.1835. If violated, the next area to provide support could be around 1.1745.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals