Summary

- Revised data show that real GDP grew at an annualized rate of 6.4% in Q1-2021, which is unchanged from the initial estimate that was released a month ago.

- The overall rate of real GDP growth was driven by broad-based increases in many of the underlying spending components.

- Gross domestic income grew at a robust rate of 6.8%, boosted in part by stimulus checks and supplemental unemployment benefits that were included with the fiscal relief packages signed into law in December and March.

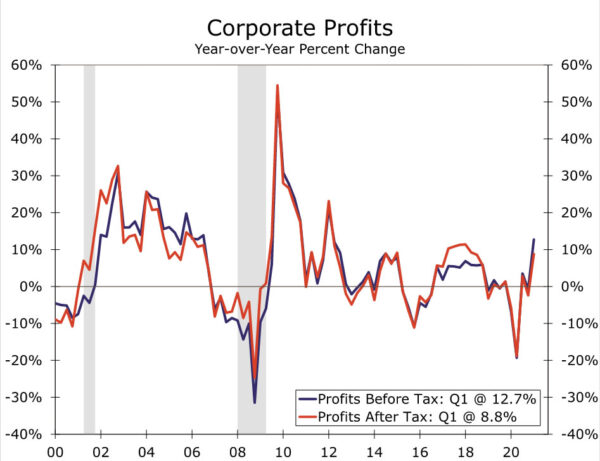

- Corporate profits were roughly unchanged during the quarter, but advanced 12.7% on a year-ago basis as comparisons were flattered by the start of pandemic-related declines in the first quarter of last year.

- Profit margins slipped to 10.4%, but remain elevated from a historical perspective and suggest firms have some room to absorb increased costs, if they so choose.

- The profit data came in largely as we had forecast, and we continue to look for profit growth to pick up this year along with overall GDP.

Demand-Side Drivers of Growth Were Broad Based in Q1

Revised data released this morning show that real GDP grew at an annualized rate of 6.4% in the first quarter relative to Q4-2020, which was unchanged from the first estimate of GDP growth that was released a month ago (Figure 1). Revisions to the individual spending components of GDP were generally immaterial. Real GDP growth in Q1 was driven by the 11.3% rise in personal consumption expenditures. But the demand-side drivers of real GDP growth in the first quarter were broader than just consumer spending. Specifically, non-residential fixed investment grew 10.8% due to strong growth in business spending on equipment and software (13.4%) and intellectual property (16.9%). Residential fixed investment posted its third consecutive double-digit increase in the first quarter, and government spending rose 5.8%. In short, the economy appears to be hitting on most cylinders at present.

In that regard, the economy continues to climb out of the hole it fell into last year. Real GDP plunged more than 10% between Q4-2019 and Q2-2020, the steepest downturn since the Great Depression. But three consecutive quarters of positive growth has left the level of GDP just 0.9% shy of its pre-pandemic peak. Most economic indicators suggest that real GDP will easily surge past its previous peak in the current quarter.

Income Boosted by Transfer Payments, Corporate Profits Stall Unlikely to Last

Today’s release contained the first look at gross domestic income (GDI) in the first quarter. GDI aggregates all of the income that was produced in the economy and, in theory, should be equivalent to GDP. In practice, however, the two measures often diverge somewhat due to errors and omissions in the data (Figure 2). Real GDI grew at an annualized rate of 6.8% in Q1-2021. In nominal terms, wages and salaries grew at an impressive annualized rate of 8.7% in the first quarter. Strong growth in aggregate wages and salaries reflects robust gains in employment gains—the economy added 1.539 million jobs during the first quarter—as well as strong growth in average wages. But income was also boosted by the $1.5 trillion (not annualized) worth of transfer payments in the first quarter. Some of these transfer payments reflects the stimulus checks and the supplemental unemployment benefits that were part of the fiscal relief packages signed into law in December and March.

Corporate profits are one of the components of GDI, and they remained roughly unchanged in the first quarter. Pre-tax profits declined a modest $0.2 billion, which translates to a 12.7% year-ago gain, as profits were flattered by the start of pandemic-related declines in the first quarter of last year. As seen in Figure 3, the level of profits remains high, and roughly 26% ahead of its Q2-2020 trough.

Although profit detail at the industry level is not released until the third estimate of first quarter GDP, we can tell from the macro level data that profit growth was held back by foreign profits, or remittances from foreign subsidiaries less remittances of American subsidiaries to foreign parents, and domestic financial profits. Foreign profits declined $9 billion while financial profits fell $4 billion. These declines were offset by a $12 billion gain in profits of domestic nonfinancial industries, which typically account for a bulk, or nearly 60%, of corporate profits. We expect the underlying industry detail will reveal continued growth in manufacturing and goods industries reflecting a surge in sales volume throughout the period as exhibited by the upwardly-revised personal consumption estimates for the quarter. Over the course of the year, profits should be boosted more directly by services industries as we expect consumer spending to transition back to the much-larger services category.

Pre-tax profits as a share of GDP, a proxy for corporate profit margins, slipped to 10.4% in the first quarter, which is roughly in line with pre-pandemic levels (Figure 4). Margins still remain elevated from a historical perspective and suggest firms have some cushion to rely on amid the increased costs many businesses are currently facing associated with both physical inputs and labor. But as we expect rising costs associated with the reopening of the economy to further stoke inflationary pressure this year, firms should gain more flexibility to pass increased costs onto consumers and even more meaningfully raise wages.

Despite little change in profits in the first quarter, we continue to look for profit growth to pick up this year along with overall GDP. Our latest forecast has real GDP rising 7.0% for 2021 as a whole and corporate profits advancing roughly 13%.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals