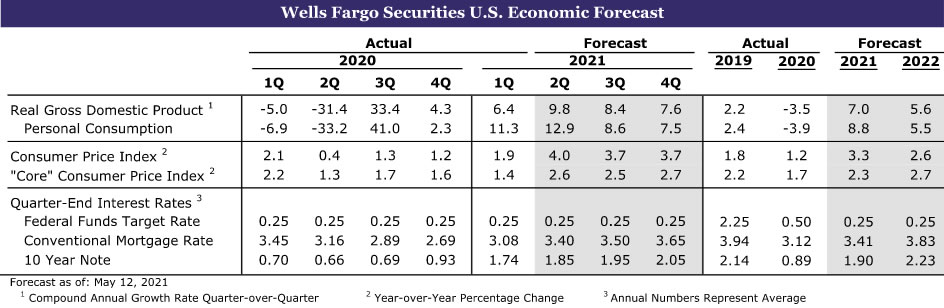

Summary

United States: Supplies Attack

- Napoleon famously observed that an army marches on its stomach; in a similar vein, an economy can grow only as fast as its supply chains.

- Material shortages were evident in the ISM reports, and the May jobs report revealed labor shortages. Employers added 559K jobs, which was short of expectations. The fact that average hourly earnings jumped again points to the fact that employers are paying up to find talent.

International: Emerging Markets Growth Outperforming Early

- Q1 GDP prints were mixed this week as Canadian data underwhelmed relative to consensus expectations, while the Brazilian and Indian economies proved to be more resilient despite COVID-related headwinds.

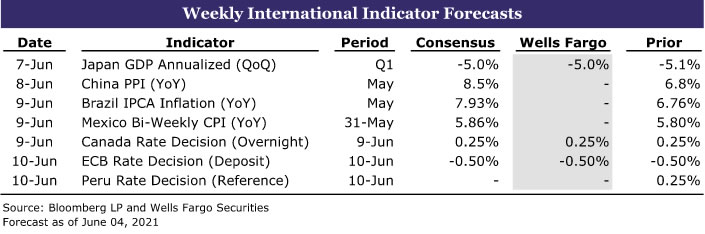

- Next week: Brazil Inflation (Wednesday), Mexico Bi-Weekly CPI (Wednesday), Peru Elections (Sunday)

Interest Rate Watch: Will the ECB Start to Taper?

- The European Central Bank holds a widely anticipated policy meeting next week. Will the Governing Council announce a “tapering” in the pace of its asset purchases?

Credit Market Insights: So Long, SMCCF

- The Federal Reserve announced this week that it plans to wind down its corporate debt portfolio. The Secondary Market Corporate Credit Facility has roughly $14 billion in corporate bonds and corporate bond ETFs, and the unwinding of this portfolio is unlikely to have much direct impact on the broader corporate bond market.

U.S. Review

Short on Supplies

The CDC’s relaxation of its mask mandate occurred mid-May, and as data for that month begins rolling in this week, it is evident there is no lack of demand. Supplies, on the other hand, are a worsening problem. Napoleon famously observed that an army marches on its stomach; in a similar vein, an economy can grow only as fast as its supply chains. The message from this week’s economic data is that it is not enough to overcome a pandemic and provide federal relief to households and businesses for the past 15 months, the global flow of raw materials and input components needs to be restored in order for this or any modern economy to run at full steam.

This was evident in the ISM manufacturing survey that kicked off the data flow at the start of this holiday-shortened week. This bellwether of industrial activity exceeded consensus expectations coming in at 61.2 in May, half a point higher than the prior month. The subcomponents moved in both directions. The story that emerges is one of a manufacturing sector that could be growing much faster were it not for supply-side growing pains.

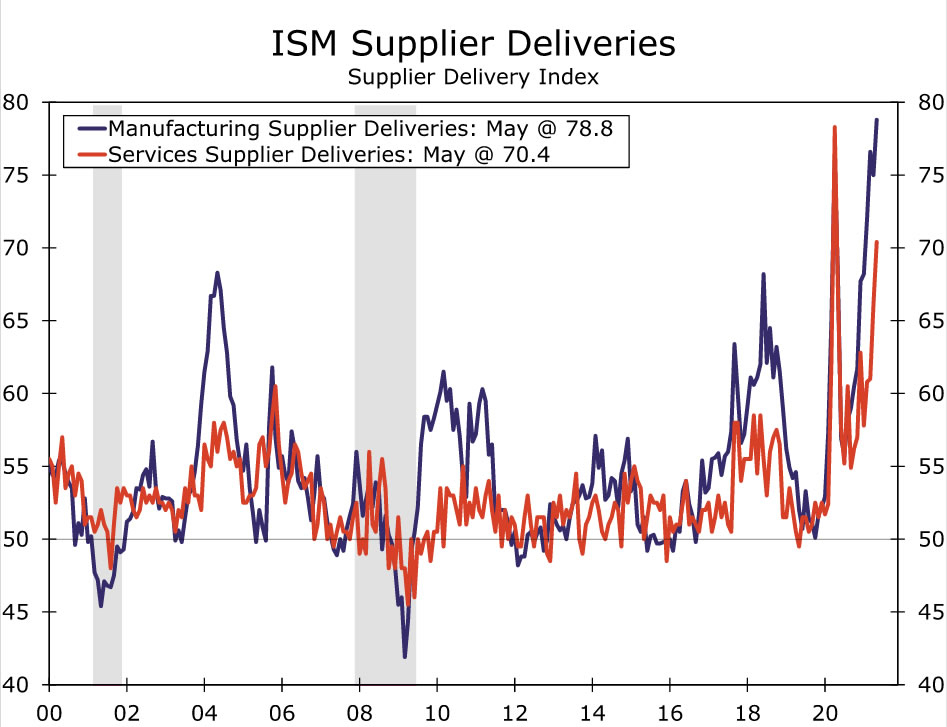

Supplier deliveries in May reached their highest level since 1974. Long wait times are having a predictable effect on output; the production index fell to 58.5 from 62.5. While any figure north of 50 signals expansion, the slowing in this measure has to be infuriating for factories that are seeing a once-in-a-lifetime demand surge, but are unable to take full advantage of it for lack of parts. This was captured in one of the featured respondents who said, “demand is strong, but what good is that if you cannot get the materials needed to produce your finished goods?” Price pressures remained front and center, with the prices paid index coming in at 88.0 in May and scarcity keeping a bid on limited supplies.

Service Sector Best Since at Least the 1990s Amid Labor Scarcity

In figures going back to the late 1990s, service sector activity has never been so strong and broad based. The services ISM shot up to a record high of 64.0 in May. It is increasingly apparent that manufacturers are not the only ones cursing the fact that they cannot source the materials they need. The supplier deliveries subcomponent in this week’s services ISM rose to 70.4, a figure exceeded only in the midst of last year’s lockdowns. Here too, we see demand is outstripping scarce supply, pushing the prices paid component to the second-highest reading on record. While some service industries, like finance and insurance, are not particularly parts-reliant, many are. Note that the ISM counts among services companies industries like construction, wholesale trade, transportation & warehousing as well as retail trade and mining.

It is difficult to overstate the degree of euphoria across various industries within the service sector. 100% of industries report overall growth, 100% of industries report increasing business activity, 100% of industries saw an increase in new orders…and 100% of industries report paying higher prices.

Contributing to upward price pressures are ongoing challenges to restaff after the pandemic. The employment components of both ISM measures slipped in May in a harbinger of what was to come with Friday’s disappointing jobs report.

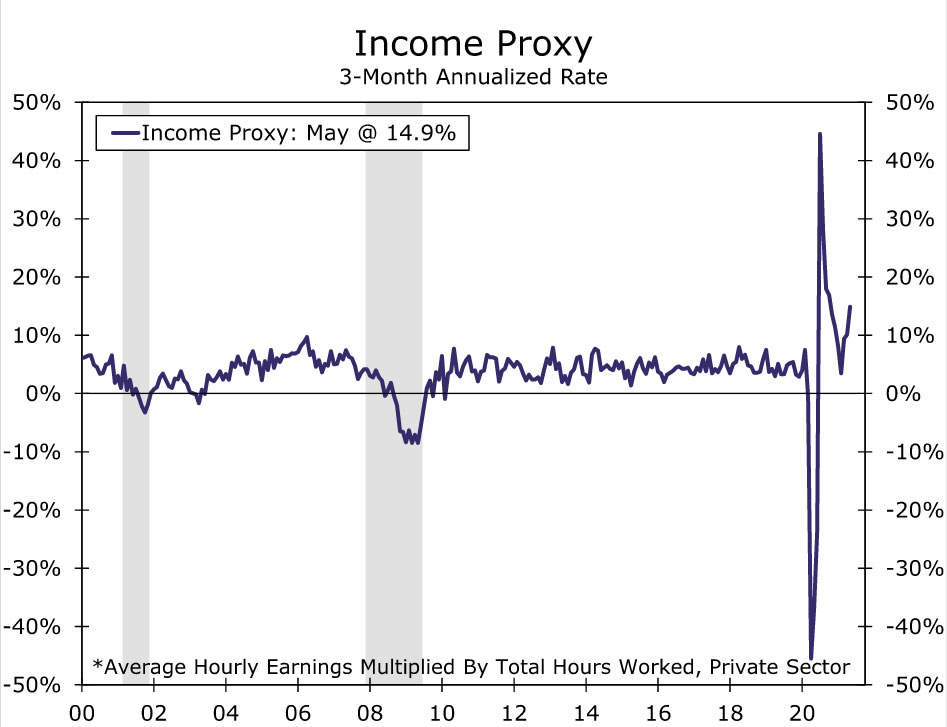

Employers added 559K new workers to nonfarm payrolls in May, and while that was a near doubling of the prior month’s gain, it fell short of expectations for even faster hiring. Demand for labor is clearly strong, as evidenced by record job openings, elevated hiring plans and a leap in consumers viewing jobs as plentiful. But finding workers remains a clear hurdle to hiring. The fact that average hourly earnings increased more than double what was expected and is way above pre-pandemic trend points to the fact that materials are not the only things in short supply. The length of the average workweek has been trending higher as well. Our income proxy in the nearby chart multiplies average hourly earnings by total hours worked. The cost of labor is rising at a nearly double-digit percentage pace.

U.S. Outlook

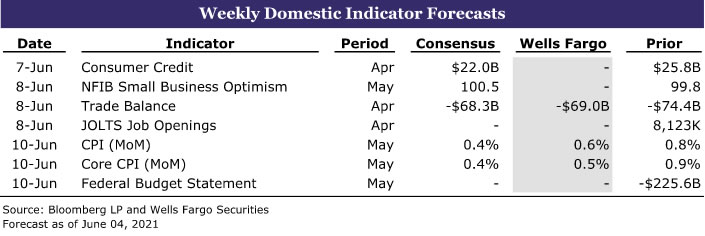

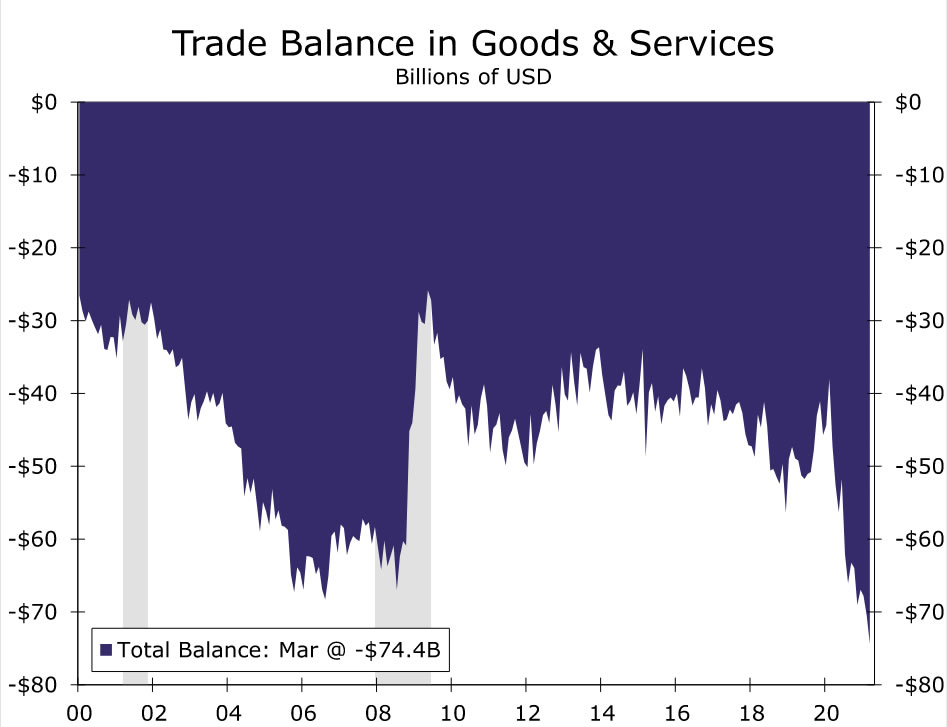

Trade Balance • Tuesday

After reaching a record deficit in March, we forecast the U.S. trade balance narrowed to a deficit of $69.0B in April. According to the advanced goods trade report, goods exports rose 1.2%, while goods imports slipped 2.2%. The advanced data suggest weaker import growth than we were previously accounting for, and if the April trade report comes in as we forecast, it would present upside risk to our currently published estimate for net exports to subtract 1.3 percentage points from Q2 GDP growth.

Trade continues to be disrupted by supply problems. Autos were a source of weakness for both exports and imports in April as supply chain constraints continued to wreak havoc on the sector. In addition to autos, advanced data suggest consumer goods trade was weak after considerable strength in March. Weakness on the exports side was offset by the second consecutive month of strong gains in capital goods and a solid gain in industrial supplies exports, as the global manufacturing sector begins to find firmer footing. Services trade likely continued its recovery in April and is set to move higher this year as the sector reopens. Trade should continue to ebb and flow in the coming months as businesses restock inventories and bottlenecks work themselves through the supply chain.

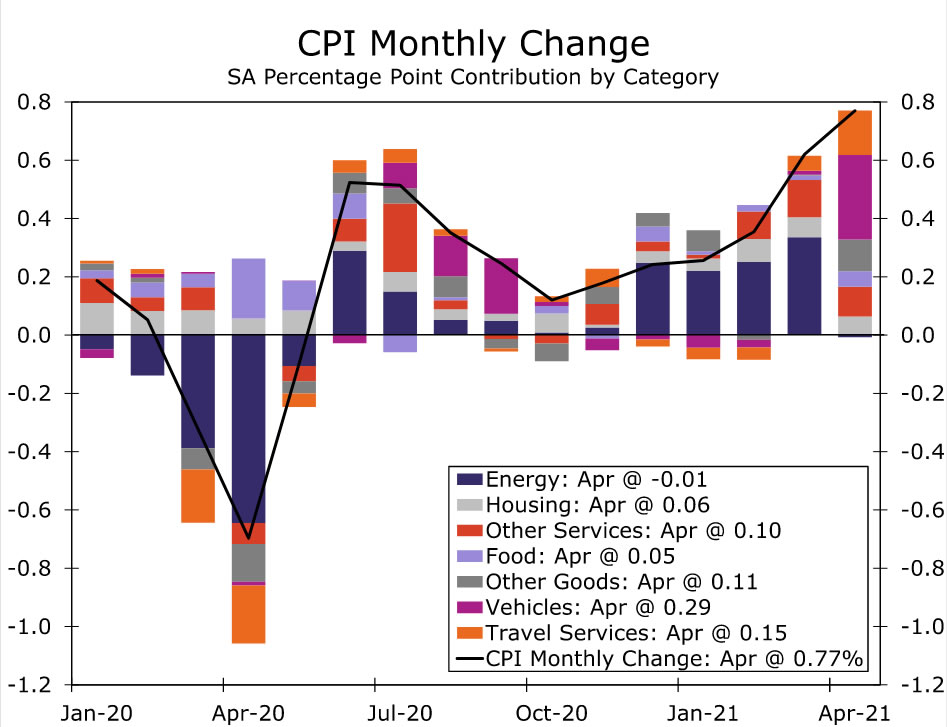

Consumer Price Index (CPI) • Thursday

We expect prices firmed further in May and forecast the CPI rose 0.6%. If realized, this would push the year-ago comparison to 4.9%, the highest since 2008. Price gains were likely broad based, and we expect to see the core index rose 0.5% in May, lifting the year-ago comparison to 3.6%.

The overall inflation story continues to be driven by increasingly constrained supply and the reopening of the service sector. These dynamics are giving way to price pressure for both goods and services, and prices likely moved higher across a number of categories in May. Some categories that saw large price gains in April, and drove the overall gain in the CPI, like used autos and travel services (hotel rates, car rentals and airfares), are also positioned to move higher in May.

A weaker-than-expected gain in prices may allay some fears that inflation is about to spiral out of control. But even if prices rise more than we forecast, we do not think it will push the Fed off its current easy policy path. The Fed has deemed the recent surge in prices as transitory and will wait to see how the dust settles on inflation and inflation expectations before changing course.

International Review

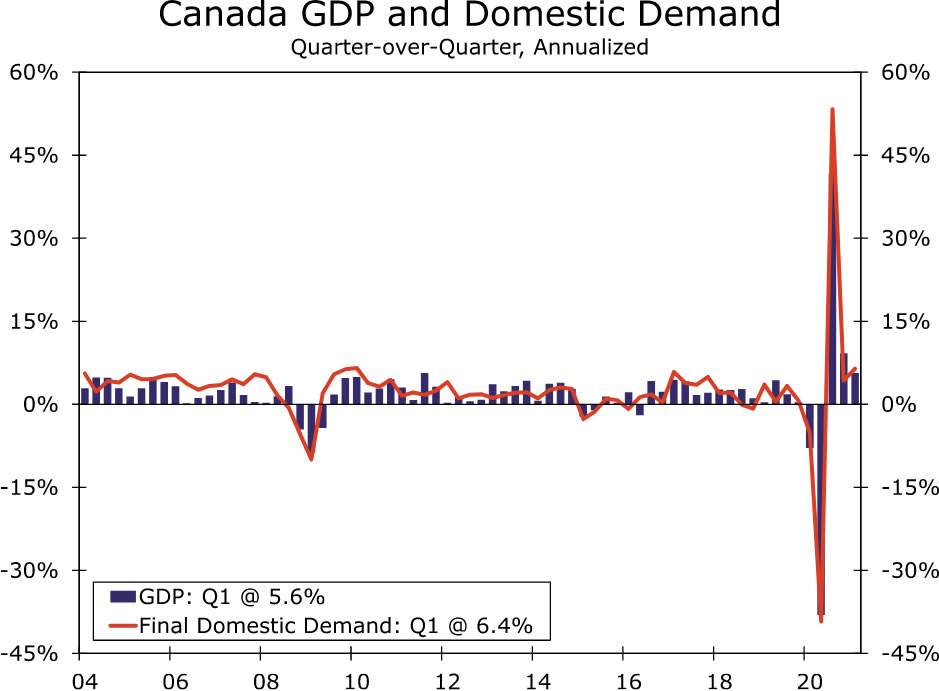

Canadian GDP Falls Short

This week, Canada reported Q1-2021 GDP data that fell short of consensus expectations. On an annualized basis, the Canadian economy grew 5.6% versus a consensus forecast of 6.8%. The miss in GDP can largely be attributed to a renewed spread of COVID cases earlier in the year that put a damper on household consumption. Spending on services slowed as businesses in some parts of the country closed, weighing on overall output in the first quarter. Despite the undershoot, there are some bright spots. Goods spending rose in Q1, while residential investment remains strong on favorable financing conditions. In addition, oil prices continue to push higher, which can support the economy over the course of this year, especially as restrictions continue to be lifted.

Despite the downside miss in Q1, we remain optimistic on the prospects for the Canadian economy as well the Canadian dollar. Local COVID cases are receding and should allow for increased mobility, while the Canadian economy has demonstrated a fair degree of resilience throughout the pandemic up to this point. This resiliency has allowed for the Bank of Canada to taper its asset purchase program and begin to signal to financial markets that interest rate hikes could be coming in the not too distant future. To that point, we expect the Bank of Canada to continue tapering asset purchases over the course of this year and, once completed, lift its key policy rate. We expect policy rate hikes to materialize in the second half of 2022, which would make the Bank of Canada one of the first major G10 central banks to raise interest rates. Tighter monetary policy has helped the Canadian dollar to be one of the top performing developed market currencies this year. In our view, an economy that should remain supported over the course of the year, combined with tighter monetary policy, can continue to result in a stronger Canadian dollar relative to the greenback.

Emerging Markets Growth Outperforming Early

Early this week, Brazil reported Q1 GDP data that beat expectations by a relatively wide margin. In Q1-2021, the Brazilian economy grew 1.2% quarter-over-quarter and 1% year-over-year, both data points higher than our forecast and consensus expectations. With the spread of COVID and restrictions a major concern in Brazil, expectations were for a more subdued GDP print to start the year. However, the economy proved more resilient as sectors such as agriculture drove the economy, while investment into Brazil also supported growth during the quarter. Going forward, the economy could pick up steam as additional household support in the form of cash handouts was implemented toward the end of the first quarter and should support consumption activity in Q2 and beyond. As far as our 2021 GDP forecast, the outperformance in Q1 certainly tilts the risk around our forecast to the upside. In the coming days, we will provide a more specific update to our Brazil GDP forecast, although a preliminary analysis suggests our forecast could be revised higher to reflect possible growth of around 5% this year.

Resiliency was also a theme across Q1 GDP data in India as the economy also outperformed relative to expectations. The COVID crisis in India has been well documented and will likely have a catastrophic impact on the local economy; however, it seems as if the effects of COVID were not felt in Q1. In fairness, India’s second wave of infections began in March and restrictions in New Delhi and Mumbai followed a few weeks later, likely pushing the economic impact more into Q2 and possibly Q3. The Indian economy expanded 1.6% year-over-year in the first quarter against a consensus forecast of just 1% growth.

Despite a more resilient economy in Q1, we expect Q2 data to tell a different story. State restrictions across the country have been harsh and could result in another quarterly economic contraction. New COVID cases may have peaked and turned a corner; however, most restrictions are still in place and a migration out of India’s larger cities and business hubs is still under way. We have revised our 2021 GDP forecast lower a few months in a row to reflect evolving conditions, and while Q1 data were better than we expected, it is very likely Q2 and Q3 forecasts get revised lower again in the coming days. The downward revisions could offset the outperformance in Q1 and our GDP forecast is likely to suggest growth of 10.5% for calendar year 2021.

International Outlook

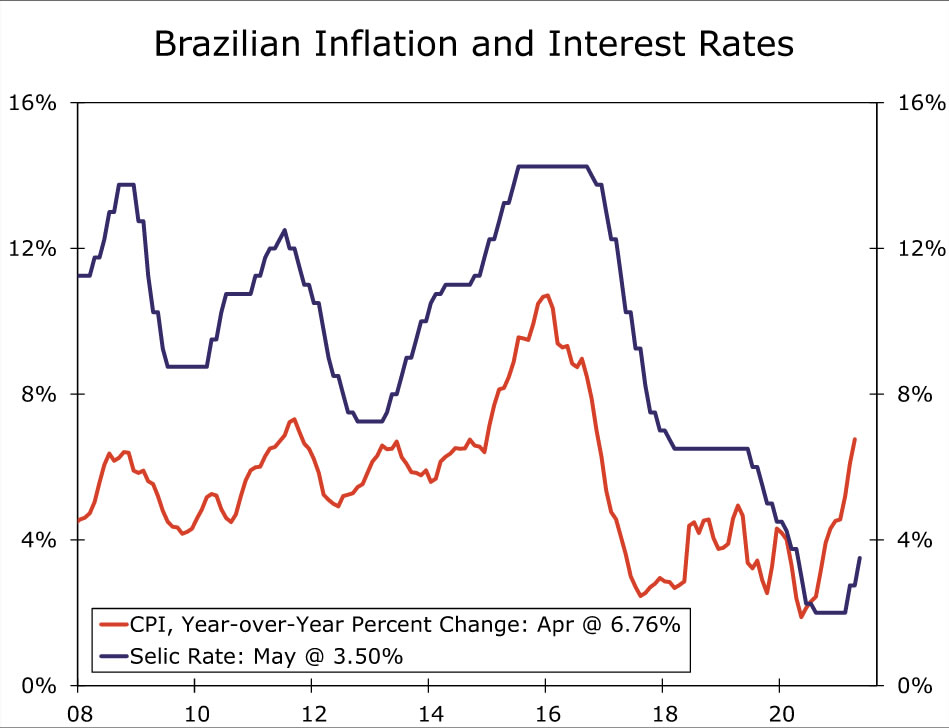

Brazil IPCA Inflation • Wednesday

The combination of aggressive fiscal stimulus, a persistently weak currency and elevated commodity prices has pushed inflation in Brazil to levels not seen since 2016. Despite 150 bps of rate hikes from the Brazilian Central Bank (BCB) this year, inflation continues to rise and remains on an upward trajectory. To that point, consensus forecasts expect inflation to reach 7.93% year-over-year in May, well above the upper bound of the BCB’s target range. As inflation continues to move higher over the course of the year, we have consistently revised our annual inflation forecast higher. As of now, we forecast annual 2021 inflation in Brazil to hit 5.5%, although risks around this forecast are tilted toward greater price growth than we expect.

As inflation moves higher, we believe the BCB will look to tighten monetary policy at a more aggressive pace. Following the guidance it laid out at its latest meeting, we believe the Selic rate will be lifted another 75 bps at the next meeting. By the end of the year, we expect additional rate hikes as well, all in an effort to contain inflation and provide much needed stability to the Brazilian currency.

Mexico Bi-Weekly CPI • Wednesday

Inflation across the emerging markets has been pushing higher for most of this year as economic recoveries gather momentum and commodity prices push higher. CPI in Mexico is no exception as inflation has moved well above the upper bound of the central bank’s inflation target. As of now, bi-weekly CPI in Mexico is 5.80% year-over-year, much higher than the Central Bank of Mexico’s 4% upper-bound target. Consensus forecasts expect inflation to increase next week as well, while the central bank has also commented that CPI may not be as transitory as it initially expected. To that point, the central bank’s quarterly inflation report showed a sharp upward revision to its annual inflation forecast, another signal inflation may remain above target for an extended period.

In our view, higher inflation is likely to result in policy rate hikes from the Central Bank of Mexico by the end of this year. A weak peso should also contribute to the central bank’s decision to tighten monetary policy, while rate hikes from peer central banks could also be a factor when Banxico assesses monetary policy over the second half of this year. As of now, Mexico’s policy rate stands at 4.00%, and we expect rates to rise to 4.25% by the end of 2021.

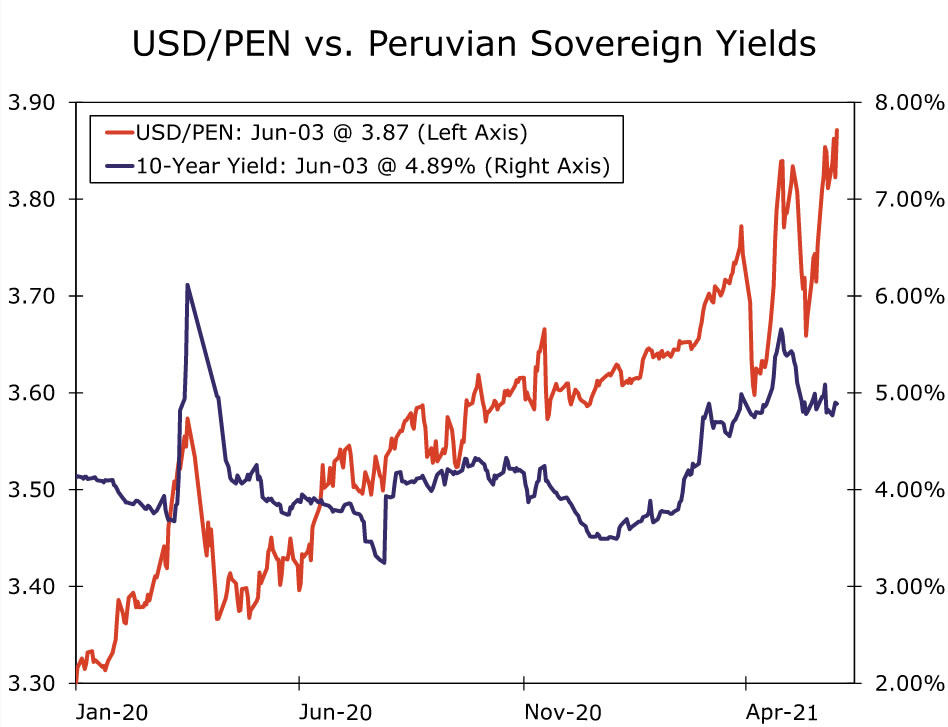

Peru Presidential Election • Sunday

On Sunday, Peruvians will head to the polls to elect a new president as well as members of Congress. For decades, Peruvian politics have been complicated, to say the least, and heading into this weekend’s election, the status of local politics is as complex as ever. Multiple presidents have been impeached or resigned over the past few decades, and in late 2020, another term was ended due to impeachment, while his immediate successor was forced to resign. The impact of COVID has added another challenge to this year’s election as protests across Lima and other parts of the country erupted in response to a perceived inadequate response to the spread of the virus.

The candidates in this weekend’s runoff election are on complete opposite ends of the political spectrum—Pedro Castillo, the former teacher and self-proclaimed Marxist, and Keiko Fujimori, a pro-business candidate and daughter of the currently jailed former president. Initially, polls showed Castillo had a massive lead; however, the lead has narrowed, and as of now, it is widely considered to be a toss up. Uncertainty around the election has roiled Peruvian financial markets and taken the currency to historical lows. If Castillo wins, expect the currency and sovereign debt to sell off sharply, while a Fujimori win could result in a relief rally for Peruvian asset prices.

Interest Rate Watch

Will the ECB Start to Taper?

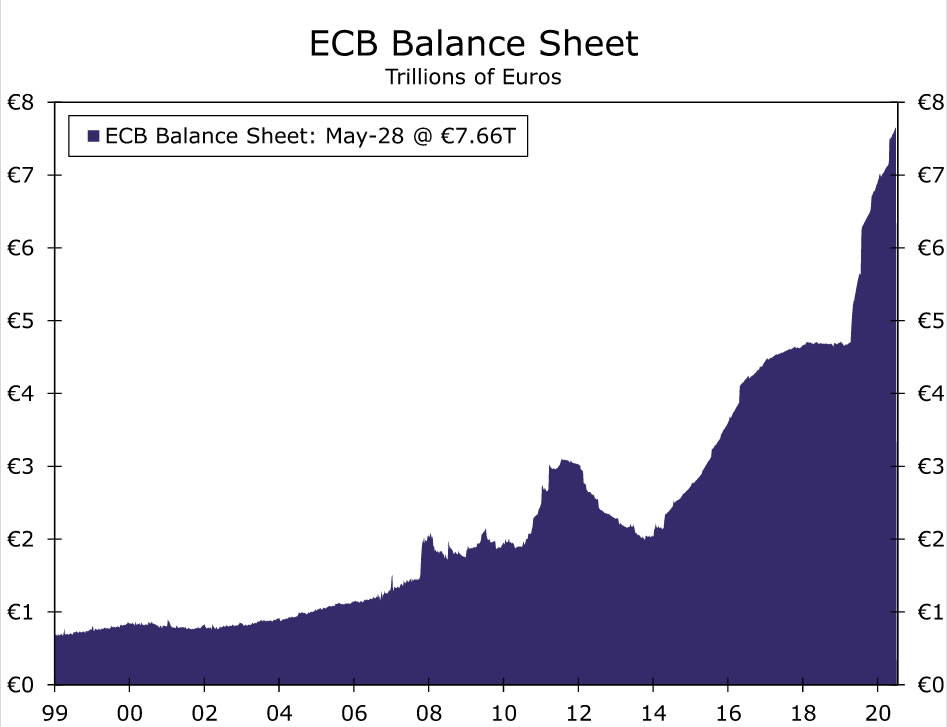

The European Central Bank holds a widely anticipated policy meeting on Thursday, June 10, but chances are slim that the Governing Council will make any changes to its three policy rates at its upcoming meeting. The Governing Council has maintained its two-week refinancing rate, which is its main policy rate, at 0.00% since March 2016, and most observers, including us, expect it to remain unchanged well into the future. The bigger question is what, if anything, the Governing Council will do about its asset purchases.

As shown in the chart, the size of the ECB’s balance sheet has exploded since the pandemic began due to a number of asset purchase programs that the Governing Council has implemented. One of these programs, the Pandemic Emergency Purchase Program (PEPP), authorizes the ECB to purchase up to €1.850 trillion worth of assets. The ECB has used up about 60% of this authorization so far.

Will the Governing Council announce a “tapering” in the pace of its asset purchases? On one hand, the pandemic appears to be receding as the pace of vaccinations has ramped up in many European economies. Incoming data suggest that economic activity in the euro area is accelerating, which calls into question the need for further monetary accommodation. On the other hand, however, the level of real GDP in the Eurozone remains more than 5% below its pre-pandemic peak, and the core rate of CPI inflation is only 0.9% at present.

We think that it would be premature for the Governing Council to announce a tapering in its asset purchases at its June 10 meeting. In our view, most ECB policymakers want to see unmistakable signs that a self-sustaining economic recovery is under way in the Eurozone before starting the process of dialing back the pace of asset purchases. We think it is more likely that the ECB will announce a tapering in its asset purchases later this year.

But if the Governing Council gives clues on June 10 that a tapering of asset purchases is at hand, then financial markets would likely react. Specifically, yields on government bonds, which have trended higher since the beginning of the year, likely would rise further. The euro could also strengthen on indications that the ECB is getting ready to slow the pace of monetary support. Stay tuned.

Credit Market Insights

So Long, SMCCF

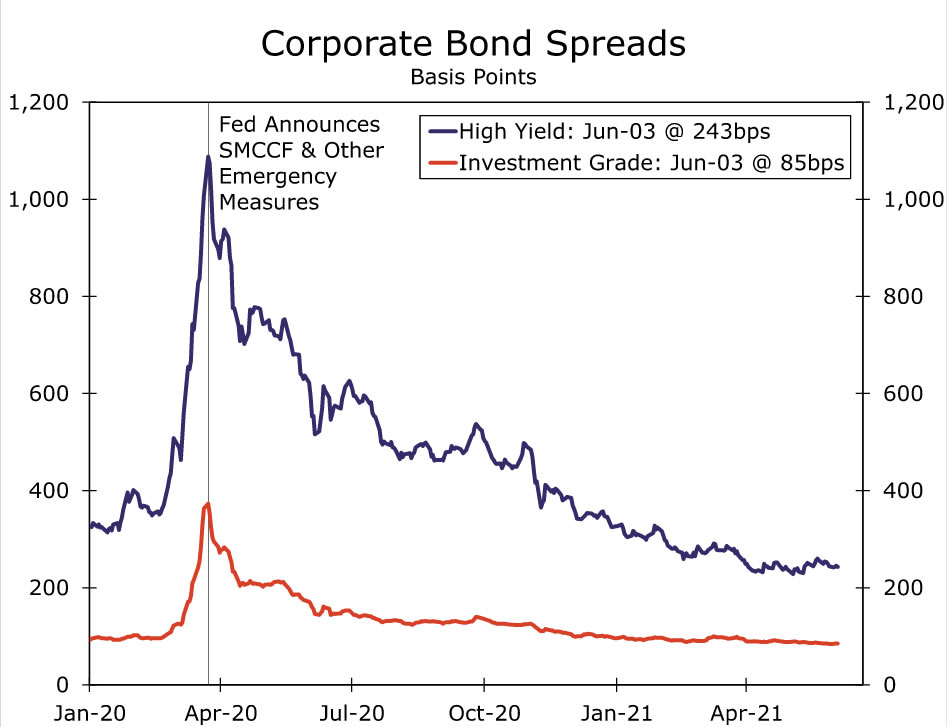

The Federal Reserve announced this week that it plans to wind down its corporate debt portfolio starting next week. The Secondary Market Corporate Credit Facility (SMCCF) was one of the many programs announced in March of last year that aimed to stabilize reeling financial markets and reopen lending channels. Many of these programs saw relatively little take up. Currently, the SMCCF has roughly $14 billion in corporate bonds and corporate bond ETFs, and the unwinding of this portfolio, which the New York Federal Reserve expects to complete by year-end, is unlikely to have much direct impact on the broader corporate bond market.

While the corporate credit facilities did not ultimately purchase many bonds, the Fed’s willingness to weigh in to the corporate bond market was sufficient to shift sentiment. Corporate bond spreads, or the premium companies pay to borrow relative to the benchmark 10-year U.S. Treasury, tightened meaningfully in the wake of the announcements on March 23, even as the broader economic outlook continued to deteriorate. The Fed did not expand its eligibility criteria to high-yield bonds until April or purchase any securities until May, but by then, the medicine had already started to take.

The reaction to the Fed pulling away has been muted thus far. While this may seem to be a sign that the Fed is ready to pull away its support for markets more broadly, the Fed has done little to connect the closing of these facilities to the path of its more traditional policy measures. Moreover, the SMCCF already ceased new purchases at the end of last year, and the timeline for closing these emergency facilities was always much shorter than the timeline for traditional QE. What the establishment of these facilities means for the next crisis remains an open question, however. While policymakers have emphasized that the extraordinary measures undertaken last year were proportional to the unprecedented pandemic-induced downturn, it is unclear to what extent these assurances will be sufficient to dissuade markets from expecting similar support in the next downturn.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals