It’s a relatively quiet summer week for global markets. The only central bank meeting will be in Australia, where the Reserve Bank could take the first step towards exiting cheap money. In America, the minutes of the latest FOMC meeting will shed some light on when the Fed might take its own foot off the accelerator. Overall, the theme of monetary policy divergence will likely dominate the FX arena moving forward.

Exit strategy

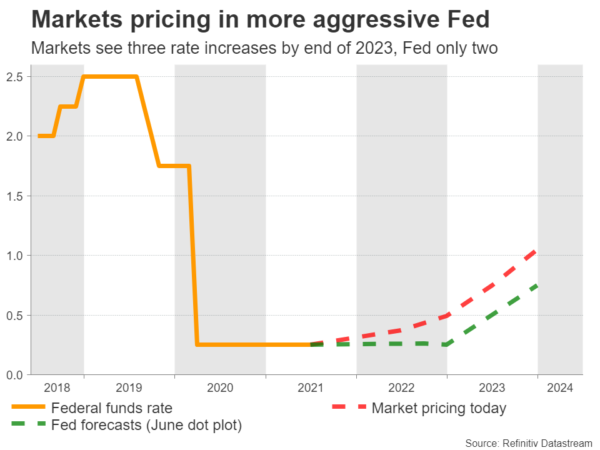

The dollar has returned to life these past few weeks, as markets absorb the fact that the era of free money is coming to an end. The US economic engine is firing on all cylinders and Fed officials are worried that if they keep their foot on the gas too long, it could overheat. Better to step on the brakes a little now, than being forced to pull the handbrake later.

As such, it looks like the Fed will cut back on its asset purchases later this year. This tapering decision could be taken in September already, after a strong warning signal in August. Beyond that, markets are pricing in the first rate increase for late 2022, with another two in 2023.

But it’s not just the Fed. The central banks of the UK, Canada, and New Zealand have all taken baby steps in the same direction. In fact, markets think New Zealand will be the first to raise rates, with that move being fully priced in for February.

In contrast, Japan and Switzerland won’t normalize anytime soon. The recovery has been slow in both economies, with Japan still battling deflation. The European Central Bank is also in this camp, but not to the same extent. The economy is doing better and some believe the ECB could dial down its asset purchases too. Even so, it won’t raise rates for a long time. Indeed, it might raise its inflation target soon, essentially committing to negative rates for longer.

Adding everything up, it looks like monetary policy divergence will become a dominant theme over the next year or so. The economies that will be raising interest rates could see their currencies appreciate against those that won’t, setting the stage for some powerful FX moves.

Aussie braces for tricky RBA

On Tuesday, we’ll find out where Australia falls between these two camps. The Reserve Bank will announce its latest decision and there is speculation that it could take the first step towards exiting cheap money too. But it will be tricky.

On the bright side, the economy is strong. For example, the unemployment rate fell to 5.1% in May, even though government support programs ended. The RBA’s latest forecasts expected that to happen around December. Meanwhile, business surveys remain optimistic, the housing market is booming, and the prices of commodities that Australia exports are high.

The catch is that vaccinations have been slow and half the country is now back in a lockdown after new clusters of infections popped up in major cities. The shutdown is only expected to last a couple of weeks and infections are still low, but this is still worrisome.

As for the market reaction, it will depend on two elements. Will the RBA repeat that rates won’t rise until 2024, and will it roll its bond purchases forward another six months to confirm its commitment to its yield curve control strategy? If the answer to both is yes, the aussie will tank. If it is no, it will jump as markets prepare for normalization.

It’s a tough one to predict. Until a week ago, it looked like the answer to both was no. But with the new lockdown, the RBA might go for the cautious ‘middle of the road’ solution – signal slower QE purchases but repeat that rates probably won’t rise until 2024, negating the market impact.

Fed minutes eyed as taper draws closer

Over in America, the ball will get rolling with the ISM services survey on Tuesday, before all eyes turn to the minutes of the latest FOMC meeting on Wednesday. The ISM index is expected to cool but remain elevated, signaling that the powerful spell of US growth continues.

Turning to the minutes, this was the meeting when the Fed shocked markets by signaling that asset purchases might be scaled back, so investors will look for clues around that. What kind of progress does the Committee want to see before taking the next step? Assuming the labor market continues to heal, it seems like the Fed will announce tapering in the autumn.

Asset purchases are just not effective anymore. The Fed’s reverse repo facility hit a new record of around $1 trillion this week, which in simple terms means liquidity is already being drained from the system. Banks are overflowing with cheap money and are giving it back to the Fed for a tiny interest rate. Why would the Fed keep printing aggressively just so it gets that money back a few hours later?

The days of QE are probably numbered, which ultimately argues for a higher dollar/yen.

Barrage of data also on the radar

On the data front, the most crucial release will be Canada’s employment report on Friday. The latest shutdowns in Canada likely kept a lid on the labor market, but with vaccination rates being high, the outlook for the economy remains bright. As for the loonie, it could take comfort in a more hawkish central bank, US spending spilling over, and roaring oil prices.

In the UK, monthly economic growth data for May are out Friday. Cable got knocked down lately as the dollar came back to life, yet the pound has been stable against the euro and yen. With a powerful recovery allowing the Bank of England to normalize faster than the ECB or BoJ, sterling could shine against the euro and yen over time.

Finally, China’s inflation stats for June will also hit markets on Friday. The focus will be on producer prices, which are seen as a proxy for global factory demand.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals