Overall, the forex markets are relatively mixed today and trading will probably continue to be subdued with US on holiday. Sterling is currently the stronger one, followed by Yen and Aussie. Canadian is the weakest, followed by Kiwi and then Swiss. Eurozone is mixed despite strong investor sentiment data. But all major pairs and crosses are staying inside Friday’s range. Some volatility could finally be seen again, especially in Aussie, with RBA rate decision scheduled in the upcoming Asian session.

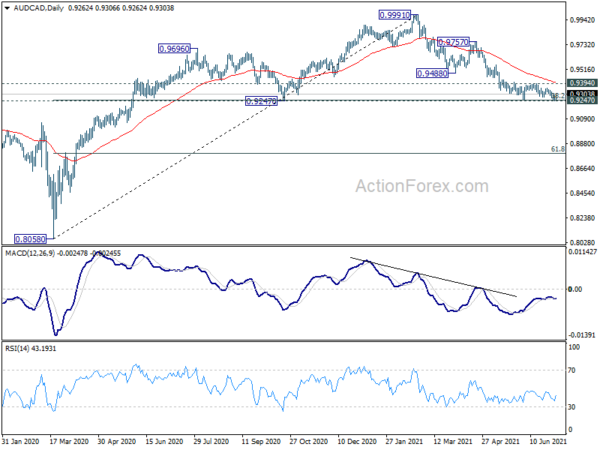

Technically, it looks like AUD/CAD has defended 0.9247 key support again. Further rebound tomorrow, subject to RBA’s decision and statement, could pop the cross back towards 0.9394 resistance. Firm break there will complete a double bottoming pattern (0.9258, 0.9245), and turn near term outlook bullish. We’ll see if that would happen.

In Europe, at the time of writing, FTSE is up 0.52%. DAX is up 0.05%. CAC is up 0.35%. Germany 10-year yield is up 0.0232 at -0.211. Earlier in Asia, Nikkei dropped -0.64%. Hong Kong HSI dropped -0.59%. China Shanghai SSE rose 0.44%. Singapore Strait Times rose 0.39%. Japan 10-year JGB yield dropped -0.0104 to 0.036.

Eurozone Sentix investor confidence rose to 29.8, but expectations dropped

Eurozone Sentix Investor Confidence rose to 29.8 in July, up from 28.1, but missed expectation of 30.2. Nonetheless, it’s still the 5th increase in a row, and highest since February 2018. Current situation index rose from 21.3 to 29.8, 5th increase in a row, and highest since October 2018. Expectations index, however, dropped from 35.3 to 29.8, lowest since December 2020.

Sentix said, “the result is impressive” but, “we are approaching a certain point of maximum momentum in the short term” as expectations dropped. “For the economy as a whole, this is not yet a worrying decline. For the equity markets, on the other hand, which are very much focused on investor expectations, this development could contribute to increased market volatility.”

It added, “in this environment, the ECB remains in focus. So far, there is no sign of a turn away from the expansive monetary policy. However, the inflation barometer, which remains clearly in negative territory at -38.25, underscores the danger of further rising inflation rates in a globally increasingly synchronised, strong economic upswing.”

Eurozone PMI composite reached 16-yr high, recovery stepped up a gear, but inflationary pressures ratcheted higher

Eurozone PMI Services was finalized at 58.3 in June, up from May’s 55.2. PMI Composite was finalized at 59.5, up from May’s 57.1. That’s also the highest level in 15 years since June 2006. Looking at some member states, Ireland PMI composite dipped to 2 month low at 63.4. Spain hit 256-month high at 62.4. Germany hit 123-month high at 60.1. Italy reached 41-month high at 58.3. France also reached 41-month high at 57.4.

Chris Williamson, Chief Business Economist at IHS Markit said: “Europe’s economic recovery stepped up a gear in June, but inflationary pressures have also ratcheted higher… A wave of optimism that the worst of the pandemic is behind us has meanwhile propelled firms’ expectations of growth to the highest for 21 years, boding well for the upturn to gain further strength in coming months.

“Firms are increasingly struggling to meet surging demand, however, in part due to labour supply shortages, meaning greater pricing power and underscoring how the recent rise in inflationary pressures is by no means confined to the manufacturing sector. Service sector companies are hiking their prices at the steepest pace for over 20 years as costs spike higher, accompanying a similar jump in manufacturing prices to signal a broad-based increase in inflationary pressures.”

UK PMI services finalized at 62.4, composite at 62.2

UK PMI Services was finalized at 62.4 in June, down slightly from May’s 62.9. That’s still the second-highest reading since October 2013. PMI Composite dropped to 62.2, down from 62.9. That’s also the second-highest reading since January 1998.

Tim Moore, Economics Director at IHS Markit: “The service sector recovery remained in full swing during June as looser pandemic restrictions released pent up demand for business and consumer services. Sales growth eased slightly from May’s recent peak, but capacity constraints and staff shortages meant that many service providers struggled to keep up with new orders…

“The latest survey data highlighted survey-record rates of input cost and prices charged inflation across the service sector, reflecting higher commodity prices, transport shortages and staff wages. Imbalanced supply and demand was the main driver, while the roll-back of pandemic discounting by some service providers amplified the latest round of price hikes.”

BoJ upgraded economic assessment of 2 regions, downgraded 2, kept 5 unchanged

In the Regional Economic Report, BoJ upgraded economic assessment of 2 regions (Hokuriku and Kinki), downgraded 2 regions (Chugoku and Shikoku), and kept 5 regions unchanged (Hokkaido, Tohoku, Kanto-Koshinetse, Tokaiand Kyshu-Okinawa).

It added: “while they reported that their economy had remained in a severe situation due to the impact of the novel coronavirus (COVID-19) — with some reporting that it had seen a slowdown in the pace of its pick-up — many reported that it had picked up as a trend or had started to pick up.”

Governor Haruhiko Kuroda told branch managers, “Japan’s economy remains in a severe state but is picking up as a trend… As the pandemic’s impact gradually eases, the economy will recover thanks to increasing external demand, loose monetary policy and the effect of government stimulus measures.”

Australia retail sales rose 0.4% mom in May, impacted by Victorian lockdown

Australia retail sales rose 0.4% mom, 7.7% yoy in May. That’s an upward revision to preliminary result of 0.1% mom rise.

Ben James, Director of Quarterly Economy Wide Surveys, said: “The main themes from the Retail Trade Preliminary release remain relevant for the Final release. Retail turnover in May was impacted by the Victorian lockdown from May 28 onwards, as well as those states recovering from restrictions in April.”

Australia AiG construction dropped to 55.5, facing capacity constraints

Australia AiG Performance of Construction dropped -2.8 pts to 55.5 in June. Current activity dropped -0.9 to 54.8. Employment dropped -6.1 to 58.3. New orders rose 0.9 to 56.1. Supplier deliveries dropped -8.5 to 50.9. Input prices rose 2.5 to 98.3. Selling prices rose 7.0 to 85.2. Average wages rose 5.4 to 70.4.

Ai Group Head of Policy, Peter Burn, said: “Australia’s construction industry continued its run of strong growth in June but the pace of expansion is slipping as it faces capacity constraints and rising input prices.”

Also released, building permits dropped -7.1% mom in May, versus expectation of -5.0% mom.

China Caixin PMI services dropped to 50.3, PMI composite dropped to 50.6

China Caixin PMI Services dropped to 50.3 in June, down from 55.1, well below expectation of 55.7. There were the softest increase in activity and new work for 14-months. Staff numbers fell as capacity pressured eased. Rates of input cost and output charge inflation slowed notably. PMI Composite dropped to 50.6, down from 53.8, worst in 14-month.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, activity in both the manufacturing and services sector continued to expand. However, impacted by the resurgence of the virus in some regions in China, the services sector was weaker than the manufacturing sector, both in terms of market supply and demand or employment.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1823; (P) 1.1849; (R1) 1.1890; More…

Outlook in EUR/USD remains unchanged and intraday bias stays neutral first. Further fall is expected as long as 1.1974 resistance holds. Break of 1.1806 will resume the decline from 1.2265, as the third leg of the consolidation pattern from 1.2348, to 1.1703 support. On the upside, break of 1.1973 resistance will turn bias back to the upside for 1.2265 resistance.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. Reaction from 1.2555 should reveal underlying long term momentum in the pair. However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index Jun | 55.5 | 58.3 | ||

| 1:30 | AUD | Retail Sales M/M May | 0.40% | 0.10% | 0.10% | |

| 1:30 | AUD | Building Permits M/M May | -7.10% | -5.00% | -8.60% | -5.70% |

| 1:45 | CNY | Caixin Services PMI Jun | 50.3 | 55.7 | 55.1 | |

| 7:45 | EUR | Italy Services PMI Jun | 56.7 | 56 | 53.1 | |

| 7:50 | EUR | France Services PMI Jun F | 57.8 | 57.4 | 57.4 | |

| 7:55 | EUR | Germany Services PMI Jun F | 57.5 | 58.1 | 58.1 | |

| 8:00 | EUR | Eurozone Services PMI Jun F | 58.3 | 58 | 58 | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Jul | 29.8 | 30.2 | 28.1 | |

| 8:30 | GBP | Services PMI Jun F | 62.4 | 61.7 | 61.7 | |

| 14:30 | CAD | BoC Business Outlook Survey |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals