Dollar’s rally continued last week as supported by hawkish comments from Fed officials. Expectations for tapering this fall continued to build up. Swiss Franc is trading broadly lower, as the pull back against Euro accelerated. Meanwhile, Australian is also trading lower on poor business confidence data. Focus will turn to Germany economic sentiment first, with an eye on any more comments from Fed officials.

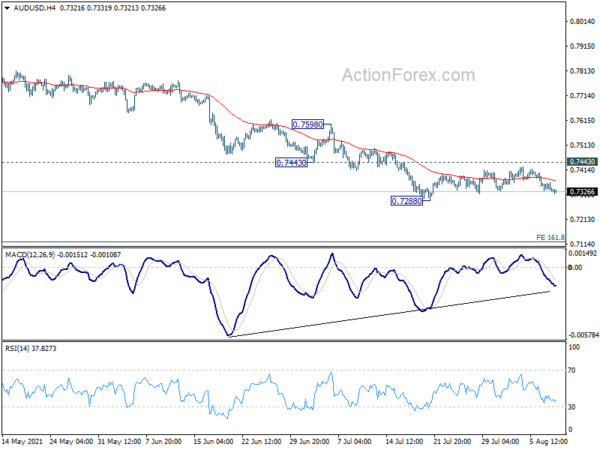

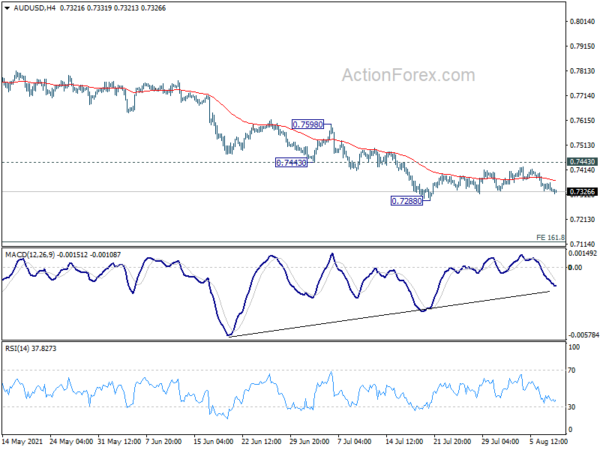

Technically, while Dollar’s rally continued, the strength against commodity currencies and Sterling is not too apparent yet. AUD/USD would have to break through 0.7288 low to show Dollar’s underlying strength. Also, USD/CAD will have to break through 1.2605 minor resistance while GBP/USD will have to break through 1.3766 minor support. Otherwise, Dollar’s rally is still a bit half-hearted.

In Asia, Nikkei closed up 0.25%. Hong Kong HSI is up 0.75%. China Shanghai SSE is up 0.52%. Singapore Strait Times is up 0.69%. Japan 10-year JGB yield is up 0.0094 at 0.024. Overnight, DOW dropped -0.30%. S&P 500 dropped -0.09%. NASDAQ rose 0.16%. 10-year yield rose 0.027 to 1.317, back above 1.3 handle.

Fed Bostic thinking about Oct-to-Dec range on tapering

Atlanta Fed President Raphael Bostic said yesterday, “we are well on the road to substantial progress toward our goal”, and July’s 943k job growth was “definitely quite encouraging in that regard.”

“My sense is if we are able to continue this for the next month or two I think we would have made the ‘substantial progress’ toward the goal and should be thinking about what our new policy position should be,” he said.

“Right now I’m thinking in the October-to-December range, but if the number comes back big” as with the last report “or maybe even a little bigger, I’d be open to moving it forward,” Bostic said. “If the number really explodes, I think we would have to consider that.”

Also, he said he favored a “balanced” approach on tapering both the MBS and treasuries purchases at the same fate, and “going relatively fast”. “The economy is in a much different place today” and “I am pretty confident these markets are going to continue to function even with a more rapid withdrawal, and I would be willing to lean into that to try to get us to complete the taper in a shorter period than what we have done in previous rounds.”

Fed Rosengren: More substantial job gains would imply tapering this fall

Boston Fed President Eric Rosengren said yesterday if the US continues to have job growth like the last two months, with “very substantial payroll employment gains”, then by September meeting, the “substantial further progress” criteria should be met. That would “imply starting to taper sometime this fall”.

“If you continue to purchase assets, the reaction primarily is in pricing, not so much in employment,” he added. “I don’t think asset purchases are having the desired impact on really promoting employment.”

Australia NAB business confidence dropped to -8, conditions dropped to 11

Australia NAB business confidence dropped sharply from 11 to -8 in July. Business conditions dropped form 25 to 11. Looking at some details, trading conditions dropped form 32 to 12. Profitability conditions dropped from 25 to 6. Employment conditions dropped from 18 to 10.

NAB said: “The continuing lockdown in NSW and the briefer periods of disruption across a number of other states saw a further deterioration in activity in the business sector in July… Confidence took a big hit in the month with optimism collapsing on the back of ongoing restrictions.”

“It is now widely expected that we will see a negative print for GDP in Q3. However, we know that once restrictions are removed that the economy has tended to rebound relatively quickly. We will continue to track the survey very closely for an indication of just how quickly that happens – particularly forward orders and capacity utilisation as we assess how the disruption has fed into expansion plans as conditions bounce back”.

Elsewhere

UK BRC like-for-like retail sales rose 4.7% yoy in July, below expectation of 7.2% yoy. Japan Eco Watcher sentiment rose to 48.4 in July, above expectation of 42.9.

Looking ahead, Germany ZEW economic sentiment is the major focus in European session. US will release non-farm productivity and unit labor costs later in the day.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7317; (P) 0.7340; (R1) 0.7353; More…

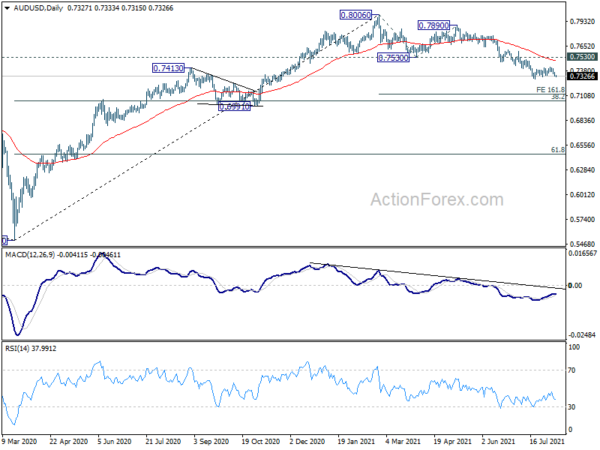

AUD/USD drops mildly but stays in consolidation from 0.7288. Intraday bias remains neutral for the moment. Outlook stays bearish as long as 0.7443 resistance holds. On the downside, break of 0.7288 will resume the fall from 0.8006 to 161.8% projection of 0.8006 to 0.7530 from 0.7890 at 0.7120 next. On the upside, break of 0.7443 will bring stronger rebound to 0.7530 support turned resistance instead.

In the bigger picture, rise from 0.5506 medium term bottom could have completed at 0.8006, after failing 0.8135 key resistance. Correction from there could target 0.6991 cluster support (38.2% retracement of 0.5506 to 0.8006 at 0.7051). We’d look for strong support from there to bring rebound. However, sustained break of this level would argue that the whole medium term trend has indeed reversed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Jul | 4.70% | 7.20% | 6.70% | |

| 1:30 | AUD | NAB Business Confidence Jul | -8 | 11 | ||

| 1:30 | AUD | NAB Business Conditions Jul | 11 | 24 | ||

| 5:00 | JPY | Eco Watchers Survey: Current Jul | 48.4 | 42.9 | 47.6 | |

| 9:00 | EUR | Germany ZEW Economic Sentiment Aug | 57 | 63.3 | ||

| 9:00 | EUR | Germany ZEW Current Situation Aug | 30 | 21.9 | ||

| 9:00 | EUR | Eurozone ZEW Economic Sentiment Aug | 72 | 61.2 | ||

| 10:00 | USD | NFIB Business Optimism Index Jul | 102.3 | 102.5 | ||

| 12:30 | USD | Nonfarm Productivity Q2 P | 3.60% | 5.40% | ||

| 12:30 | USD | Unit Labor Costs Q2 P | 1.20% | 1.70% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals