Euro tumbles notably against European majors and Yen today, and ECB’s re-calibration of PEPP purchases provide no support. But Dollar is seen as equally weak. Sterling is currently the star performer for today, followed by Swiss Franc and Yen. Commodity currencies are mixed. Focuses will now turn back to development in stocks and bonds markets, as both look relatively soft.

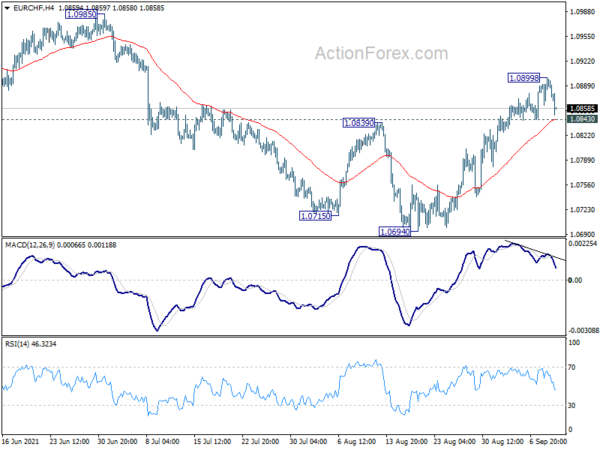

Technically, EUR/GBP’s sharp fall and strong break of 0.8561 support argues that rebound from 0.8448 might have completed at 0.8612 already. Well ahead of 0.8668 resistance. Deeper fall would now be seen back to retest 0.8448 low. Eyes will be on 1.0843 support in EUR/CHF. Break there will also suggest completion of rebound from 1.0694. Also, firm break of 1.1792 support in EUR/USD would bring retest of 1.1663 low.

In Europe, at the time of writing, FTSE is down -1.06%. DAX is up 0.11%. CAC is up 0.12%. Germany 10-year yield is down -0.0129 at -0.336. Earlier in Asia, Nikkei dropped -0.57%. Hong Kong HSI dropped -2.30%. China Shanghai SSE rose 0.49%. Singapore Strait Times rose 0.09%. Japan 10-year JGB yield dropped -0.0058 to 0.040.

ECB: Favorable financing conditions can be maintained with moderate lower pace of PEPP

ECB kept the envelope of the Pandemic Emergency Purchase Programme (PEPP) unchanged at EUR 1850B, and will continue purchases until at least the end of March 2022. Nevertheless, the Governing Council now “judges that favourable financing conditions can be maintained with a moderately lower pace of net asset purchases under the PEPP than in the previous two quarters.” ECB will now “purchase flexibly” according to market conditions, over time, across assets classes and among jurisdictions.

Also, ECB kept main refinancing rate, marginal lending rate and deposit rate unchanged at 0.00%, 0.25%, and -0.50% respectively. Forward guidance is maintained, which imply a transitory period of overshoot. The regular asset purchase program will also continue at a monthly pace of EUR 20B.

In the post meeting press conference President Christine Lagarde said the rebound phase in the recovery of Eurozone economy is “increasingly advanced”. Output is expected to exceed its prepandemic level by the end of the year. Current rise in inflation is expected to be “largely temporary”. Medium term inflation is “foreseen to remain well below our two percent target”. Risks to economic outlook is “broadly balanced”.

In the new economic projections ECB raised 2021 growth forecasts from 4.6% to 5.0%. For 2022, GDP growth is downgraded slightly form 4.7% to 4.6%. 2021 GDP growth was forecast was kept unchanged at 2.1%.

Inflation forecast was revised slightly up, from 1.9% to 2.2% in 2021, from 1.5% to 1.7% in 2022, and from 1.4% to 1.5% in 2023.

US initial jobless claims dropped to 310k, pandemic low

US initial jobless claims dropped -35k to 310k in the week ending September 4, better than expectation of 343k. Four-week moving average of initial claims dropped 16.75k to 339.5k. Both were the lowest level since March 14, 2020.

Continuing claims dropped -22k to 2783k in the week ending August 28, lowest since March 14, 2020. Four-week moving average of continuing claims dropped -29k to 2840k, lowest since March 21, 2020.

Fed Bostic: Recent weaker data suggests a chance for some play on tapering

Atlanta President Raphael Bostic “as strong as the data was coming in the early part of the summer, I was really very much leaning into advocating for an earlier start than what many may have expected”.

However, “the weaker data that we’ve seen more recently suggests to me that maybe there’s a chance for some play on this, but I still think that sometime this year is going to be appropriate” to taper.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8571; (P) 0.8587; (R1) 0.8596; More…

EUR/GBP’s sharp decline and break of 0.8561 support argues that rebound from 0.8448 has completed already. Intraday bias is back on the downside for retesting 0.8448 low. Also, with 0.8668 resistance defended, larger down trend is probably still in progress, starting another leg through 0.8448 low. On the upside, above 0.8612 will resume the rise form 0.8448 to 0.8668 resistance instead.

In the bigger picture, price actions from 0.9499 (2020 high) are still seen as developing into a corrective pattern. Deeper fall could be seen as long as 0.8668 resistance holds, towards long term support at 0.8276. However, firm break of 0.8668 resistance would argue that a medium term bottom was already formed. Stronger rise would be seen to 0.8861 support turned resistance to confirm completion of the corrective pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q2 | 3.90% | 2.10% | 2.70% | |

| 23:01 | GBP | RICS Housing Price Balance Aug | 73% | 76% | 79% | 77% |

| 23:50 | JPY | Money Supply M2+CD Y/Y Aug | 4.70% | 4.70% | 5.20% | 5.30% |

| 01:30 | CNY | CPI Y/Y Aug | 0.80% | 1.00% | 1.00% | |

| 01:30 | CNY | PPI Y/Y Aug | 9.50% | 9.00% | 9.00% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Aug | 86.20% | 93.40% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Jul | 17.9B | 13.3B | 13.6B | |

| 11:45 | EUR | ECB Interest Rate Decision | 0.00% | 0.00% | 0.00% | |

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | USD | Initial Jobless Claims (Sep 3) | 310K | 343K | 340K | 345K |

| 14:30 | USD | Natural Gas Storage | 38B | 20B | ||

| 15:00 | USD | Crude Oil Inventories | -5.9M | -7.2M |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals