Asian Futures:

- Australia’s ASX 200 futures are up 41 points (0.57%), the cash market is currently estimated to open at 7,280.80

- Japan’s Nikkei 225 futures are up 140 points (0.5%), the cash market is currently estimated to open at 28,423.92

- Hong Kong’s Hang Seng futures are down -27 points (-0.11%), the cash market is currently estimated to open at 23,825.24

- China’s A50 Index futures are down -50 points (-0.32%), the cash market is currently estimated to open at 15,461.16

UK and Europe:

- UK’s FTSE 100 index rose 65.92 points (0.94%) to close at 7,109.95

- Europe’s Euro STOXX 50 index rose 19.93 points (0.49%) to close at 4,109.51

- Germany’s DAX index rose 23.82 points (0.16%) to close at 15,280.86

- France’s CAC 40 index rose 36.52 points (0.54%) to close at 6,776.25

Monday US Close:

- The Dow Jones Industrial rose 263.6 points (0.68%) to close at 35,135.94

- The S&P 500 index rose 60.65 points (1.33%) to close at 4,655.27

- The Nasdaq 100 index rose 373.657 points (2.33%) to close at 16,399.24

US large cap equities were broadly higher with tech stocks leading the way. The Nasdaq rose 2.3% to take Q4’s rally to around 9%, the S&P 500 was up 1.2% ad the DJI gained 0.7%. These may be early signs of a Santa’s rally but also dovish remains from Jerome Powell also likely helped. During his testimony on coronavirus he noted “downside risks to employment and economic activity and increased uncertainty for inflation”.

Biden: Omicron is cause for concern, not panic

Following a meeting at the Whitehouse with his COVID-19 team, Joe Biden said that the Omicron variant is cause for concerns, not panic and that the US is working on contingency plans for new vaccines with pharmaceutical companies. Meanwhile the WHO said the “unprecedented number of spike of mutations” are concerning although no deaths have yet been linked to the new variant.

If nothing else, this new covid variant seems to have caught the attention it craves but the world waits with bated breath to better gauge the ramifications on the economic recovery and society as a whole.

There’s been an outage at Twitter

And that outage is Jack Dorsey, who announced he is stepping down as CEO and handing his reigns over to Parag Agrawal, the current Chief Technology Officer. Twitter (TWTR) suspended trading to announce the decision, gapped up around 10% but ultimately closed -1.7% lower.

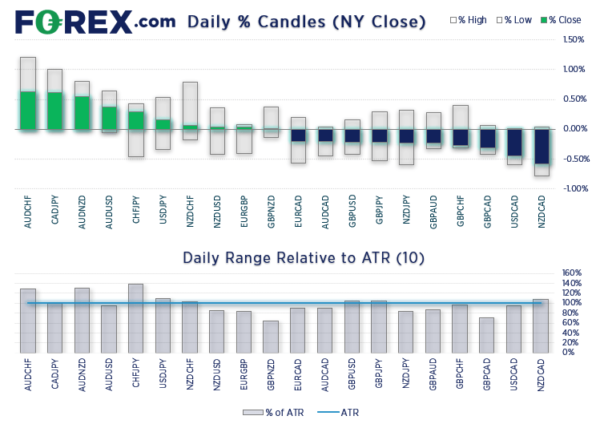

Commodity FX held onto minor gains

It would be incorrect to say the commodity currencies AUD and CAD led the session with any bullish conviction, because they did not. They simply retraced against Friday’s bearish moves by a relatively small amount. But that AUD/USD held above last week’s low (and USD/CAD pulled back from week’s high) provides a clear line in the sand in case sentiment turns, which will likely be triggered by Omicron, the new bogeyman in town. Therefore, currency markets remain in wait or see mode, as there’s no apparent reason to pile into risk or extend Friday’s sell-off with the lack of solid information available for this new covid variant.

Covid headlines to remain the main driver for markets

In all likelihood economic data might take a back seat to a degree this week, even if the calendar is full of events. But when do markets ever ‘waste a crisis’ if data comes in much weaker than expected, alongside the fear of Omicron?

At 11:30 AEDT, NZ business confidence is expected to have fallen further on October, with around net-20% of respondents expecting a weaker economy due to higher inflation. And this is already showing up in consumption with last week’s poor retail sales figures, so it’s becoming harder to justify another rate hike from RBNZ any time soon.

China’s manufacturing PMI is expected to have contracted for a third consecutive month, although at a slower pace. The data set is a familiar combination of weak exports, new orders with rising prices. And that is only going to get worse if we see further travel restrictions imposed. For today China’s headline PMI is expected to contract but at a slower pace, according to a Reuters poll.

Given lockdowns in NSW and VIC, Q3 GDP in Australia scheduled for tomorrow is expected to have contracted. And today’s net-exports contribution to GDP could help fine tune expectations by just how much. And if we get a weak print, alongside a softer China manufacturing Report (with headline below 49.2) then we’d expect AUD to come under pressure and hand back some of yesterday’s mild gains.

Potential H&S pattern on gold

A potentially interesting setup is emerging on gold. The daily chart formed a bearish pinbar yesterday which found resistance at its monthly R1 pivot before closing back beneath the 200-day eMA. The hourly chart shows as established downtrend to the 1777 lows and a potential head and shoulders top has also formed, and its right shoulder (RS) respected the 200-day eMA as resistance. Prices have since found support at the monthly pivot point but we’d take a break of 1777 support to confirm a downside breakout of the pattern. But prices need to break down relatively soon to keep the pattern alive, as a break above 1800 invalidates R and therefore the pattern potential.

ASX 200 held above 7200

The index initially fell below 7200 and reached the upper bounds of our 7145 – 7185 support zone, before paring earlier losses and only closing -0.5% lower on the day. Having recouped just under 2/3rds of losses it has left a potential ‘buying tail’ on yesterday’s candle, although bulls really need to send prices above 7311 to avoid another dip lower.

ASX 200: 7239.8 (-0.54%), 29 November 2021

- Materials (0.74%) was the strongest sector and Real Estate (-1.43%) was the weakest

- 8 out of the 11 sectors closed lower

- 5 out of the 11 sectors outperformed the index

- 200 (56.98%) stocks advanced, 0 (0.00%) stocks declined

- 51.57% of stocks closed above their 200-day average

- 40.46% of stocks closed above their 50-day average

- 14.25% of stocks closed above their 20-day average

Outperformers:

- + 7.1%-Carnival PLC(CCL.L)

- + 6.83%-WH Smith PLC(SMWH.L)

- + 6.19%-Capita PLC(CPI.L)

Underperformers:

- 1.1%-Imperial Brands PLC(IMB.L)

- 1.11%-Auction Technology Group PLC(ATG.L)

- 1.15%-Jpmorgan European Discovery Trust PLC(JEDT.L)

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals