Risk aversion is back as the main theme in the global financial markets. The crash in the US overnight has spreaded to Asia. At the time of writing, Japanese Nikkei is down -756 pts or -3.42%, being the worst performer in Asia. 10 year JGB yield also suffers another day of steep decline, down -0.020 at 0.114. It was above 0.15 just a few days ago. Hong Kong HSI is down -2.07%, China Shanghai SSE is down -1.65%, Singapore Strait Times is down -1.31%. Yesterday, DOW dropped -608.01 pts or -2.41% to 24583.42. S&P 500 lost -3.09% while NASDAQ was even worst, down by -4.43%. Treasury yield also closed sharply lower with 10 year yield down -0.042 at 3.117. However, 30-year yield was down just -0.018 at 3.346. (if you want to make money in the financial market use our forex news robot)

In the currency markets, Yen is trading as the strongest one on risk aversion, in particular considering the steep fall in Nikkei. Canadian Dollar is the second strongest as it’s still feeling the support by hawkish BoC rate hike yesterday. Meanwhile, Dollar, Australian and New Zealand are the weakest ones, together with Sterling. Dollar gets no support from known Fed hawk Mester’s comments. Euro is mixed for now after this week’s decline. But the common currency is vulnerable to further selloff on German Ifo and any dovish turn in ECB rhetorics.

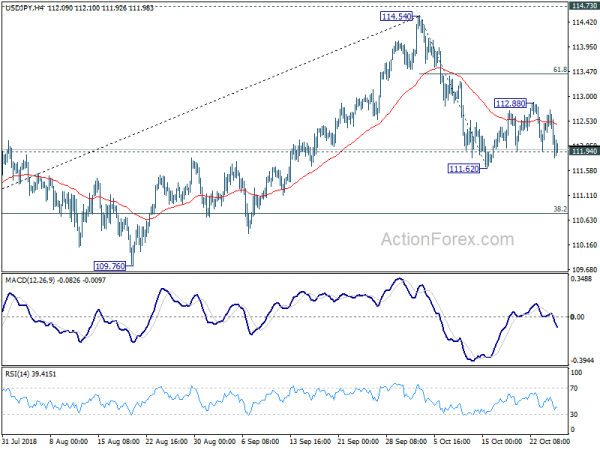

Technically, one development to note is USD/JPY has finally broke 111.94 minor support. Recent fall from 114.54 is likely resuming through 111.62 support level. EUR/USD, GBP/USD, EUR/JPY and GBP/JPY are staying bearish for further decline.

Fed Mester: Recent markets slump just a risk to outlook, no impact on fundamentals

Cleveland Fed President Loretta Mester said yesterday that recent stock market slump is just “a risk” to the economy outlook. The “fundamentals of the economy” are not affected at this point. And it doesn’t change her expectations for 3% growth this year and a little bit less next. She added the the underlying economy of the US is “strong” and there is no signs of a pending recession.

Though, she acknowledged that “prolonged downturn in the market and a pullback in risk across the board with a lowering of credit extension” would have an effect on economic data. And Fed is going to monitor the developments.

For traders: We recommend you odin forex robot free download for test in mt4 or our best Portfolio of forex robots.

Fed’s Beige Book: Tariffs getting more attentions from businesses

Fed’s Beige Book economic report warned that “manufacturers reported raising prices of finished goods out of necessity.” Such price hikes were attributed to higher raw materials costs “which they attributed to tariffs.” Though, overall inflation pressure were just “modest-to-moderate” in all districts. In the 32-page report, the word “tariff” or its derivations were mentioned a total of 51 times. And, with the exception of St. Louis, all districts made reference to tariffs one way or the other. That’s quite a sharp jump from 42 times in September.

For example, In Dallas, it’s noted that “among manufacturers, roughly 60 percent of contacts said the tariffs announced and/or implemented this year have resulted in increased input costs. The share was even higher among retailers, at 70 percent.” In Minneapolis, “a producer of dry beans reported that a large regular annual order from European Union countries was canceled due to tariffs.” In Philadelphia, “other firms reported difficulty meeting the prices of foreign competitors who are not exposed to tariffs on the primary input commodities of their products.” Read more forex news…

Canadian Dollar surged after hawkish BoC rate hike

Canadian Dollar surged sharply yesterday as the market was thrilled by BoC’s hawkish comments accompanying the widely-anticipated 25 bps rate hike. With the uncertainty of future trade relationship with the US reduced and economic growth on track, the members judged that it is prudent to move to “neutral” interest rate. Removal of the “gradual” rate hike reference, replacing by “need to rise to a neutral stance”, might be a signal that BOC would increase the policy rate at a faster pace. Policymakers noted weakness in inflation. Yet, they expect wage growth would pick up in coming quarter and would likely help boost inflation. More in BOC Review – Hiking Policy Rate to 1.75% with Hawkish Bias

Italy EM Tria: German-Italian Spread at 320 will hurt weakest parts of the banking system

Italian Economy Minister Giovanni Tria warned yesterday that German-Italian yield spread at 320 basis points is not sustainable. He noted that’s “not so much for the consequences it would have on debt interest payments”, but “for the impact it would have on the weakest parts of the banking system”. Nonetheless, on the budget rejected by European Commission, Tria insisted that the budget is correct and there is no reason to change it.

Cabinet Undersecretary Giancarlo Giorgetti also noted earlier in the week that some smaller Italian banks will needed recapitalization if the spread breaks 400 basis points. And the coalition government stands ready to intervene if that happens.

Italian 10 year yield jumps again this week after EU rejected Italy’s budget and closed at 3.617 yesterday. On the other hand, German 10 year yield is trending down on risk aversion and broke 0.40 to 0.398. Spread is currently at 321.9 as of yesterday’s close.

ECB to stand pat, may shift slightly to the dovish side due to Italy and sluggish outlook (Read fundamental analysis)

ECB rate decision and press conference is a key event for today. There shouldn’t be any chance in ECB’s monetary policy. That is, the main-refinancing rate will be held unchanged at 0.00% without a doubt. And the central bank will keep interest rates at present level at least through summer of 2019. On asset purchase program, the monthly size of purchase was reduced to EUR 15B this month and is expected to stop after December.

The main focus is ECB’s views on economic outlook and recent developments in Eurozone as well as global financial markets. ECB may emphasize downside risk to growth and that would be a slight shift from the more hawkish stance at the last meeting six weeks ago. With the path of QE announced in June, the focus is on the reinvestment arrangement. Yet, we do not expect the central bank to give much detail on the issue until the December meeting. Market volatility has recently spiked as Italy’s aggressive budget plan might violate EU’s fiscal rule and has triggered rating downgrade. We expect discussion about the issue at the press conference. There would be no new staff economic projections.

More in ECB Likely More Cautious amid Soft Core Inflation and Italy. Reinvestment Details to be Revealed in December

On the data front

New Zealand trade deficit came in larger than expected at NZD -1560m in September. Japan corporate service price index rose 1.2% yoy in September.

German Ifo business climate will catch some attention in European session along with ECB rate decision.

Later in the day, US will release trade balance, durable goods, whole inventories, jobless claims and pending home sales

NOTE: if you do not have time to search for strategies and study all the tools of the trade, you do not have the extra funds for testing and errors, tired of taking risks and incurring losses – trade with the help of our Keltner channel forex robot developed by our professionals. Also you can testing in Metatrader our forex auto scalper robot free download .

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.98; (P) 112.36; (R1) 112.63; More..

USD/JPY’s break of 111.94 minor support suggests that recovery from 111.62 has completed at 112.88 already. Intraday bias is back on the downside for 111.62. Break will resume the decline from 114.54 to 38.2% retracement of 104.62 to 114.54 at 110.75. As the fall from 114.54 is viewed as part of medium term correction, we’ll look for bottoming signal above 109.76 key support. On the upside, break of 112.88 will delay the bearish case and extend the rebound from 111.62 instead.

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.76 support holds. However, decisive break of 109.76 will dampen this bullish view and turns outlook mixed again.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals