Canadian Dollar jumps sharply in early US session after stronger than expected GDP data. At least, the three month-rolling average remained in expansion despite the contraction in December and November. Additionally, WTI crude oil surged through recent resistance to resume larger up trend to as high as 60.72. For now, New Zealand Dollar is the second strongest for today, paring some of this week’s steep losses.

Sterling is the third strongest after rebounding just ahead of near term support against Dollar and Yen. There is clearly no following through buying in the Pound as focus remains on the Brexit Withdrawal Agreement (WA) vote. It’s confirmed by EU that, approving the WA is enough for pushing Article 50 extension from April 12 to May 22. Still, it’s unsure whether there is enough votes, in particular without Northern DUP’s support. Also, only 23 Conservatives who voted against the Brexit deal confirmed they will support now, including Dominic Raab, Jacob Rees-Mogg and Boris Johnson.

Staying in the currency markets, Yen is the weakest one for today, as global stocks strengthen. Also, US 10-year yield is back up 2.4 handle at 2.42 as it enters into consolidation mode. Dollar follows as second weakest after larger than expected moderation in core PCE inflation. US Treasury Secretary Steven Mnuchin tweeted that this round of trade talks in Beijing has concluded. He described the talks as “constructive”. And he looks forward to meeting Chinese Vice Premier Liu He in Washington next week to continue the “important” discussions.

In Europe, FTSE is currently up 0.47%. DAX is up 0.93%. CAC is up 0.83%. German 10-year yield is up 0.0135 at -0.053. Earlier in Asia, Nikkei rose 0.82%. Hong Kong HSI rose 0.96%. China Shanghai SSE rose 3.20%. Singapore Strait Times rose 0.29%. Japan 10-year yield rose 0.0034 to -0.09.

Canadian Dollar jump as GDP grew 0.3% in Jan, well above expectation

Canadian Dollar jumps after stronger than expected GDP report. Real GDP grew 0.3% mom in January, well above expectation of 0.1% mom. It’s also strong enough to offset contraction in both December and November. On three month rolling average basis, real GDP edged up 0.1%, unchanged from the three-month rolling average in December. Manufacturing and construction contributed most to January’s GDP growth. Ning and oil and gas extraction contracted.

Also from Canada, IPPI rose 0.3% mom in February while RMPI rose 4.6% mom.

US core PCE inflation slowed to 1.8%, missed expectations

US personal income rose 0.2% in February, below expectation of 0.3%. It “primarily reflected increases in wages and salaries, government social benefits to persons, and proprietors’ income ”

Personal spending rose 0.1% in January, below expectation of 0.3%. It “primarily reflected decreases in personal dividend income, farm proprietors’ income, and personal interest income”

Headline PCE slowed to 1.4% yoy in January, down from 1.% yoy, matched expectation. Core PCE slowed to 1.8% yoy, down from 2.0% yoy and missed expectation of 1.9% yoy.

Swiss KOF rose to 97.4, still point to rather weak growth in coming months

Swiss KOF Economic Barometer rose to 97.4 in March, up from 93.0 and beat expectation of 93.9. The improve is predominantly due to “positive impulses” from manufacturing, as driven by the electrical industry, followed by the metal industry, mechanical engineering and the textile industry.

KOF Noted in the release that “recent downward tendency has at least for the time being ended.” However, the current reading is still “markedly below its average”. Hence, Swiss economy can expect to experience rather weak growth in the coming months.

Also from Europe…

A bunch of data is released in European session but they received little attention. UK Q4 GDP was finalized at 0.2% qoq, unrevised. Total business investment dropped -0.9% qoq, revised up from -1.4% qoq. Current account deficit narrowed to GBP -23.7B. M4 money supply rose 0.3% mom in February. Mortgage approvals dropped to 64k in February.

Germany unemployment dropped -7k in March, versus expectation of -10k. Unemployment rate dropped 0.1% to 4.9%, matched expectations. Retail sales rose 0.9% mom in February, way better than expectation of -0.9% mom. Import price index rose 0.3% mom, below expectation of 0.5% mom. Swiss KOF leading indicator improved to 97.4 in March, up from 93.0.

RBNZ Orr: Markets are forward looking and understands the central bank

RBNZ Governor Adrian Orr noted the sharp selloff in New Zealand Dollar after the central bank turned dovish earlier in Wednesday and signaled the next move in OCR is a cut. He was pleased as “markets have shown that they understand what we are focused on and they are forward looking.”

Orr explained that “what we really need is total understanding and confidence from financial markets about our goal, our determination to achieve that goal and the environment and information set we are operating within.” He added, “if financial markets watch us and we watch them then we are just looking at a mirror, we are not learning anything.

Orr said markets have to “think very hard and have their own independent mind around what we are trying to achieve. They expressed that, I assume the other day, when the currency went lower.”

Released in Asian session

Japan unemployment rate dropped to 2.3% in February, down from 2.5% and beat expectation of 2.5%. Industrial production rose 1.4% mom versus expectation of 1.3% mom. Retail sales rose 0.4% yoy versus expectation of 0.9% yoy. In March, Tokyo CPI core was unchanged at 1.1% yoy. From Australia, private sector credit rose 0.3% mom in February versus expectation of 0.2% mom. New Zealand building permits rose 1.9% mom in February.

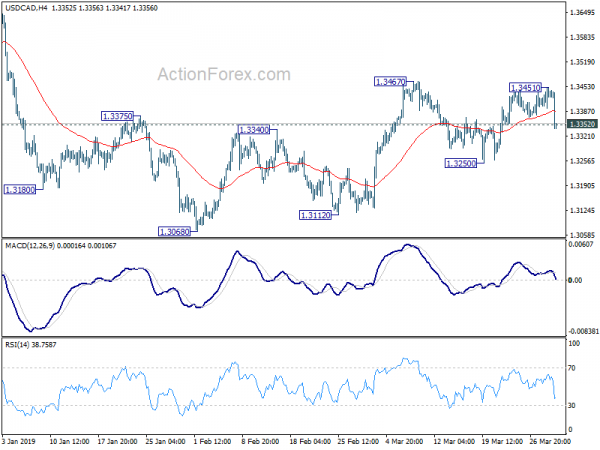

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3408; (P) 1.3431; (R1) 1.3466; More…

USD/CAD’s sharp decline and break of 1.3352 minor support suggests that rebound from 1.3250 has completed at 1.3451 already. Intraday bias is turned back to the downside for 1.3250 support. Firm break there will indicate completion of whole rebound from 1.3068. In that case, deeper fall would be seen back to 1.3068.3112 support zone. On the upside, break of 1.3467 will target a test on 1.3664 high.

In the bigger picture, structure of the medium term rise from 1.2061 (2017 low) to 1.3664 is not clearly impulsive. Hence, we’d stay cautious on strong resistance from 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 and 1.3793 resistance to limit upside, and bring medium term topping. But in any case, medium term outlook will stay bullish as long as channel support (now at 1.3192) holds. Sustained break of 1.3793 will pave the way to retest 1.4689 (2015 high). However, firm break of the channel support should confirm reversal and target 1.2061 low again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Feb | 1.90% | 16.50% | 13.60% | |

| 23:30 | JPY | Unemployment Rate Feb | 2.30% | 2.50% | 2.50% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Mar | 1.10% | 1.10% | 1.10% | |

| 23:50 | JPY | Industrial Production M/M Feb P | 1.40% | 1.30% | -3.40% | |

| 23:50 | JPY | Retail Trade Y/Y Feb | 0.40% | 0.90% | 0.60% | |

| 00:01 | GBP | GfK Consumer Confidence Mar | -13 | -14 | -13 | |

| 00:30 | AUD | Private Sector Credit M/M Feb | 0.30% | 0.20% | 0.20% | |

| 05:00 | JPY | Housing Starts Y/Y Feb | 4.20% | -0.10% | 1.10% | |

| 07:00 | EUR | German Import Price Index M/M Feb | 0.30% | 0.50% | -0.20% | |

| 07:00 | EUR | German Retail Sales M/M Feb | 0.90% | -0.90% | 3.30% | |

| 08:00 | CHF | KOF Leading Indicator Mar | 97.4 | 93.9 | 92.4 | 93 |

| 08:55 | EUR | German Unemployment Change (000’s) Mar | -7K | -10K | -21K | -20K |

| 08:55 | EUR | German Unemployment Claims Rate s.a. Mar | 4.90% | 4.90% | 5.00% | |

| 09:30 | GBP | Mortgage Approvals Feb | 64K | 65K | 67K | |

| 09:30 | GBP | Money Supply M4 M/M Feb | 0.30% | 0.30% | 0.20% | |

| 09:30 | GBP | GDP Q/Q Q4 F | 0.20% | 0.20% | 0.20% | |

| 09:30 | GBP | Total Business Investment Q/Q Q4 F | -0.90% | -1.40% | -1.40% | |

| 09:30 | GBP | Current Account Balance (GBP) Q4 | -23.7B | -22.9B | -26.5B | |

| 12:30 | CAD | GDP M/M Jan | 0.30% | 0.10% | -0.10% | |

| 12:30 | CAD | Industrial Product Price M/M Feb | 0.30% | 0.40% | -0.30% | |

| 12:30 | CAD | Raw Materials Price Index M/M Feb | 4.60% | 1.20% | 3.80% | |

| 12:30 | USD | Personal Income Feb | 0.20% | 0.30% | -0.10% | |

| 12:30 | USD | Personal Spending Jan | 0.10% | 0.30% | -0.50% | -0.60% |

| 12:30 | USD | PCE Deflator M/M Jan | -0.10% | 0.00% | 0.10% | |

| 12:30 | USD | PCE Deflator Y/Y Jan | 1.40% | 1.40% | 1.70% | 1.80% |

| 12:30 | USD | PCE Core M/M Jan | 0.10% | 0.20% | 0.20% | |

| 12:30 | USD | PCE Core Y/Y Jan | 1.80% | 1.90% | 1.90% | 2.00% |

| 13:45 | USD | Chicago PMI Mar | 61 | 64.7 | ||

| 14:00 | USD | New Home Sales Feb | 625K | 607K | ||

| 14:00 | USD | U. of Mich. Sentiment Mar F | 97.8 | 97.8 |

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals