Asian markets are mixed as another week starts. Nikkei weakens, together with Yen, as data showed the Japan economy suffered worst contraction in six years. Singapore Strait Times is also mildly lower after the government downgrade this year’s growth forecast. Yet, China and Hong Kong stocks are trading mildly higher despite continuation of Wuhan coronavirus outbreak. The currency markets are also mixed too, with Kiwi trading as the weakest while Aussie is the strongest.

Technically, Euro is losing some intraday downside momentum in a slow session. But further fall remains in favor. Levels to watch include 1.0888 minor resistance in EUR/USD, 119.55 minor resistance in EUR/JPY, and 0.8386 minor resistance in EUR/GBP. As long as these levels hold, further fall is still in favor in Euro for the week ahead.

In Asia, Nikkei is currently down -0.84%. Hong Kong HSI is up 0.38%. China Shanghai SSE is up 1.37%. Singapore Strait Times is down -0.16%. Japan 10-year JGB yield is down -0.0033 at -0.035.

China coronavirus deaths hit 1770, PBoC cut 1-yr MLF rate

According to China’s National Health Commission, on February 16, confirmed coronavirus cases in the country rose 2048 (comparing to 2009 on February 15), to 70548. Death tolls rose 105 (comparing to 142 a day ago) to 1770. Health officials said on Sunday that two days of decline in new confirmed cases affirmed the government’s effort in containing the outbreak. But data released today clearly disagree to the claim.

Outside of China, Japan is hardest hit with over 400 cases, mainly due to the numbers in Diamond Princess liner. Singapore (75 cases) and Hong Kong (57) follow. Death toll reached 5 with one new case in Taiwan over the weekend.

China’s central bank PBoC announced today to cut interest rate on its medium term loans to cushion the impact on the economy from the Wuhan coronavirus outbreak. Rate of CNY 200B worth of one-year medium-term lending facility loans is lowered by 10bps to 3.15%. Also, CNY 100B of liquidity is injected to financial institution through reverse repos. Today’s move is believed to pave the way for a cut in the benchmark loan prime rate on Thursday.

Japan GDP suffered worst b in 6 years, sentiments pessimistic

Japan GDP contracted -1.6% qoq in Q4, much worse than expectation of -0.9% qoq. In annualized term, GDP contracted -6.3%, biggest contraction in six years. Looking at some details, private consumption dropped -2.9% in response to the sales tax hike in October. Capital expenditure dropped -3.7%. External demand contributed to 0.5% point to GDP growth, in sufficient to offset -2.1% negative contribution from domestic demand. With impact from China’s coronavirus outbreak, contraction might extend into Q1, making it a technical recession.

Economy Minister Yasutoshi Nishimura said “the government had hoped Japan’s economy would continue a moderate recovery. But we must be vigilant against the impact of the coronavirus on domestic and overseas economies,”

Outlook is pessimistic too based on a Reuters survey that tracks BoJ’s Tankan. The Reuters Tankan manufacturer sentiments index rose from -6 to -5 in February. Services index rose from 14 to 15. Business confidence is not too much lifted by the US-China trade deal. The government might be forced to launch another around of fiscal stimulus soon to support growth.

Singapore downgrades 2020 growth forecasts on China’s coronavirus outbreak

Singapore government downgraded growth forecasts for the year as China’s Wuhan coronavirus outbreak is weighing on the country’s economy. For 2020, the Ministry of Trade & Industry projected growth in range of -0.5% to 1.5%, lowered from prior estimate of 0.5% to 2.5%.

Gabriel Lim, permanent secretary at the ministry, said, “as the COVID-19 situation is still evolving, there is a significant degree of uncertainty over the length and severity of the outbreak, and hence its overall impact on the Singapore economy.”

Singapore has the second highest number of coronavirus cases (75) outside China, next to Japan. Finance minister Swee Keat might launch a strong stimulus package in the budget delivered tomorrow, to offset the economic impacts.

Focuses on Eurozone sentiment on impact of coronavirus outbreak

Considering last week’s downside breakout in Euro, Eurozone data including German ZEW and more importantly, PMIs will be closely watched this week, on the impact from China’s coronavirus breakout on sentiments. Also as speculations for a ECB rate cut in the second half of the year have somewhat built up, ECB monetary policy accounts will also be watched for any clues of dovish bias.

The calendar is also busy elsewhere. UK will feature employment, inflation, retail sales and PMIs. Australia will release RBA minutes, wage price index and employment, which will be crucial to whether RBA would cut in April. Canada will also have manufacturing sales, CPI and retail sales scheduled. Most US data are second-tier but FOMC minutes will certainly catch some attentions.

- Monday: Japan GDP; UK Rightmove house price; German Buba monthly report; Canada foreign securities purchases.

- Tuesday: RBA minutes; UK employment; German ZEW economic sentiment; Canada manufacturing sales; US Empire State manufacturing, NAHB housing index.

- Wednesday: Australia wage price index; Japan machine orders, trade balance; Eurozone current account; UK CPI, PPI; Canada CPI; US PPI, housing starts and building permits, FOMC minutes.

- Thursday: New Zealand PPI; Australia employment; Swiss trade balance; German Gfk consumer climate, PPI; UK retail sales; ECB minutes; Canada new housing price index; US Philly Fed manufacturing, jobless claims; leading indicator.

- Friday: Australia CBA PMIs; Japan national CPI core, all industry index; Eurozone PMIs, CPI final; UK PMIs, public sector net borrowings; Canada retail sales; US PMIs, existing home sales.

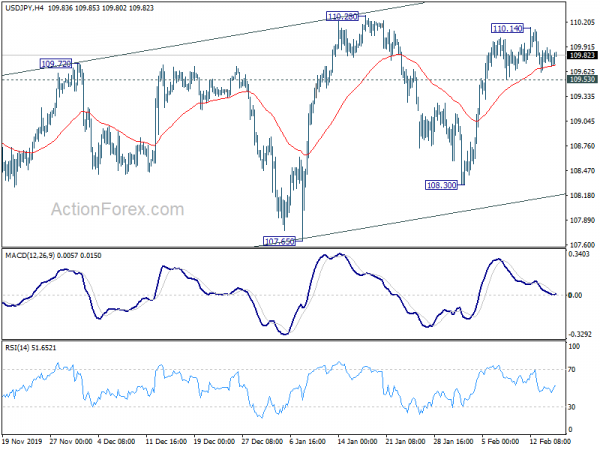

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.68; (P) 109.80; (R1) 109.89; More..

Intraday bias in USD/JPY remains neutral for the moment and further rise is in favor as long as 109.53 minor support holds. On the upside, break of 110.28 will resume whole rally from 104.45. Though, break of 109.53 will turn bias to the downside for 108.30 support instead.

In the bigger picture, there is no change in the bearish outlook yet in spite of the rebound from 104.45. The pair is staying in long term falling channel that started at 118.65 (Dec. 2016). Rise from 104.45 is seen as a correction and the down trend could still extend through 104.45 low. However, sustained break of the channel resistance will be an important sign of bullish reversal and target 114.54 resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q4 P | -1.60% | -0.90% | 0.40% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | 1.30% | 0.90% | 0.60% | |

| 0:01 | GBP | Rightmove House Price Index M/M Feb | 0.80% | 2.30% | ||

| 4:30 | JPY | Industrial Production M/M Dec F | 1.20% | 1.30% | 1.30% | |

| 9:00 | EUR | German Buba Monthly Report | ||||

| 13:30 | CAD | Foreign Securities Purchases (CAD) Dec | 4.82B | -1.75B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals