It is the mother of all weeks for the dollar and stock markets. In the aftermath of the US election, traders will have to digest a Fed meeting at 19:00 GMT Thursday and the latest US employment report at 13:30 GMT Friday. The election outcome will overshadow everything else, but we may still see some decent moves if the Fed telegraphs an increase in asset purchases come December. As for the jobs data, it is no longer a trend-setter for markets, but rather an intraday volatility event.

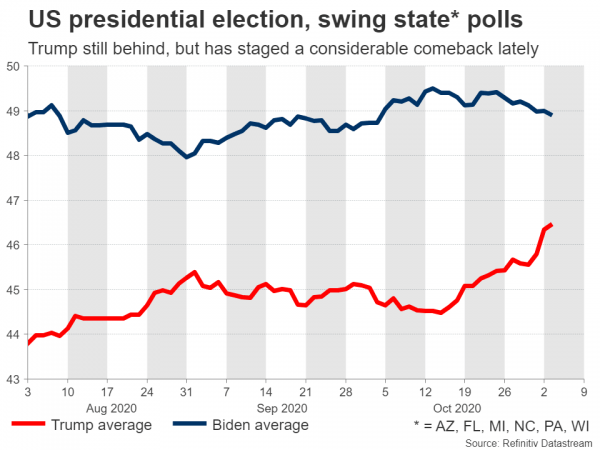

It’s not over until it’s over

There is a decent chance that we will still be counting ballots when the Fed meets on Thursday, as several swing states have allowed mail-in votes that arrive a few days late to be counted. If the result is therefore very close, the winner might not be formally announced until Thursday or even Friday.

This also implies that Trump could declare victory on election night if he is the victor with the votes that have been counted until that point, but still lose eventually as all ballots are counted, since mail-in votes tend to favor the Democrats. In this case, Trump could go on to dispute the result in the Supreme Court, throwing markets into weeks of uncertainty and dismay.

Hence, investors might have much bigger issues on their plate than the Fed or the jobs data this week, though both are always important. Even if there is a clear winner on election night, the ‘aftershock’ effects of a US election can last for several days, eclipsing other market moves.

Fed: Asymmetric event for the dollar

The Fed is unlikely to provide any fireworks. The US economy is still doing relatively fine, with the housing market booming, the latest PMIs pointing to continued recovery, and seekers of unemployment benefits declining. That said, covid infections have spiked again, and any new fiscal stimulus package will be delayed, both threatening to throw the recovery off course.

All this implies the Fed is likely to acknowledge the downside risks, but can afford to wait until December before taking any real decisions. At that point, it will have a better sense of how much damage the latest wave of infections has inflicted on the economy and how much fiscal stimulus Congress might pump.

So the real question is, will the Fed telegraph a policy move in December, like the ECB did? Admittedly, there is less urgency to do so than in Europe, even though two of the biggest downside risks have materialized – a new covid wave and no fiscal stimulus. Additionally, policymakers may not want to pre-commit to anything at this stage, for fear of disappointing later.

In the markets, if the Fed indeed signals nothing new, that would argue for a small boost in the dollar. However, this is what everyone expects already. Therefore, if policymakers surprise and do signal that more easing is coming, the downside reaction in the dollar may be much bigger. In other words, the risks surrounding the dollar from this meeting may be asymmetric, with the downside move in case of easing signals likely to be greater than the corresponding upside move in case of no easing signals.

Nonfarm payrolls: Not what it used to be

On Friday, all eyes will turn to the US jobs report for October. Nonfarm payrolls are expected to clock in at 600k, roughly in line with the 661k figure in September, pushing the unemployment rate down to 7.6% from 7.9% previously.

Admittedly though, this event is no longer as significant for markets as it used to be. The initial reaction is usually minor and fades within a few minutes, creating some volatility but not a lasting trend, even in case of substantial surprises.

Hence, the election and the evolution of covid infections may be much more important. Specifically, will we end up with a united government, where the same party controls the White House and both chambers of Congress, or not? That is likely the most crucial variable. If we do, it would be bad news for the dollar. Otherwise, the reserve currency could jump.

Election aside, relative virus trends between Europe and America matter as well. So far, Europe has been hit very hard, with the new lockdowns raising the risk that the economy contracts again in Q4. This has helped push euro/dollar a little lower, and whether this downfall continues may depend mostly on how the US performs from here.

Taking a technical look at euro/dollar, initial support to declines may be found near 1.1690, where a downside break would turn the focus to the 1.1610 zone.

On the flipside, in case of a landslide election result for example, the pair could shoot higher to challenge the 1.1720 area initially, ahead of the 1.1760 region.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals