For the most part, the US Presidential Elections are behind us and markets will turn their attention to the new November 19th Brexit “deadline” for negotiators to come up with a trade deal. Markets are hoping a deal will be in place soon in order to present it to EU leaders via their video conference on Thursday. There was plenty of excitement early last week as pharmaceutical company Pfizer announced the results of their trials, which showed its vaccine prevents 90% of corvid infections. They will seek US review later this month. However, the vaccine will not be widely available until the spring. Coronavirus daily case rates are still increasing as we approach the winter month, bringing with it more restrictions and lockdowns worldwide.

November 19th is the latest deadline for Brexit negotiations. Although both sides say progress is being made and that conversations should continue, the lack of news is leaving many traders skeptical that a deal will get done. The main issues to be resolved are the same issues that have been preventing a deal from the onset, primarily:

- An enforcement mechanism to govern the deal

- A level playing field (free and fair trade)

- Access to fishing waters surrounding the UK

As has been all along, time is of the essence. The last plenary session of the EU Parliament is December 14th-17th. These are the last days for the EU to vote on a deal. However, a deal must be reached and it needs to be reviewed by subcommittees well before that date. Upcoming notable dates are as follows:

- Nov 16th: talks to resume

- Nov 19th: EU leaders video conference

- Nov 23rd-26th: EU Parliament meeting

- Dec 10th-11th: EU leaders video conference

- Dec 14th-17th: Last EU Parliament meeting before the end of Brexit transition

However, note that if a deal isn’t reached by the end of November, the last two meetings my be focused on how to handle the no-deal Brexit, rather than how to tidy up negotiations.

In a late-day on Friday, Dominic Cummings, Boris Johnson’s right-hand man and the person who crafted Brexit, resigned. Watch GBP pairs and FTSE to see if this will affect negotiations next week.

In addition to the Brexit saga, the UK and EU must continue to deal with the ongoing coronavirus pandemic which continues to keep countries in turmoil. In the UK, the country continues to remain on lockdown. However, it may be beginning to work! Just a day after Britain became the first European country to surpass 50,000 coronavirus deaths, the R rate on Friday slowed to between 1.0 and 1.2 from between 1.1 and 1.3. The lockdown remains in effect until December 2nd. In the meantime, Chancellor of the Exchequer Sunak is working on a new stimulus plan as the BOE discusses yield curve control as they are said to be moving away from the notion of negative rates.

In the EU, most countries remain either in lockdown or under restrictions as it has been for nearly. The European Council and the European Parliament have approved the 750 billion Euro Recovery Fund; however it now must be approved by all 27 European member countries. Both Poland and Hungary are threatening to veto.

Not to take away from the severity of the situation in the EU, but the focus now turns to the US, where the CDC reported a record 194,000 new daily coronavirus cases , up from 153,000 on Thursday. President Trump has refused to issue a national shutdown, however many states have issued their own restrictions, such as curfews, occupancy limits and virtual schooling. In addition, 6 Northeastern State Governors will an emergency summit do discuss additional actions to limit the spread. Joe Biden will not take the oath of office until January 20th. Some are hoping Biden will provide more guidance from a national level in terms of restrictions and possible lockdowns than Trump has. (However, some are also hoping he won’t). The is still no signs of a US fiscal stimulus package, although hopes are that one will be passed as soon as Biden becomes President. The FOMC is on hold, waiting for more fiscal stimulus!

There was some good news last week regarding the coronavirus. Pfizer and BioNTech have announced results of a study which concluded that its vaccine prevents 90% of covid infections. They will seek US review later in November. Moderna is expecting similar results soon. Although the news is promising, first doses will go to frontline workers and may not be widely available until Q2. This means it could be a long winter. So far, stock traders are looking past the winter months as the S&P 500 is up over 9% the last 2 weeks and some stock indexes closed at all-time highs!

Earnings season is just about over, however many traders will be watching traditional retailers this week to see how the coronavirus situation has affected their bottom lines. Some of the more important earnings announcements are as follows : VOD, BHP, JD, BIDU, EZJ, HD, HLFDY, WMT, NVDA, RMG, LOW, TGT, BJ, M

The economic calendar has a few important events to take note of this week, including a China data dump on Monday, US and UK Retail sales, Australian Employment Change, Turkey’s Interest Rate Decision (which may expect a 475bps hike!), and the Philadelphia Fed Manufacturing Index (which will be our first look at November manufacturing data). Other important economic events are as follows:

Monday

- Japan: GDP Growth Rate QoQ Prel (Q3)

- China: Fixed Asset Investment YTD (OCT)

- China: Industrial Production (OCT)

- China: Retail Sales (OCT)

- China: Unemployment Rate (OCT)

- US: NY Empire State Manufacturing Index (NOV)

Tuesday

- Australia: RBA Meeting Minutes

- Canada: Housing Starts (OCT)

- US: Retail Sales (OCT)

- US: Industrial Production (OCT)

- US: Manufacturing Production (OCT)

- US: NAHB Housing Price Index (NOV)

Wednesday

- Japan: Trade Balance (OCT)

- Australia: HIA New Home Sales (OCT)

- UK: Inflation Data (OCT)

- EU: Inflation Rate Final (OCT)

- Canada: Inflation Rate (OCT)

- US: Housing Starts (OCT)

- US: Building Permits (OCT)

- Crude Inventories

Thursday

- New Zealand: PPI (Q3)

- Australia: Employment Change (OCT)

- Turkey: CBRT Interest Rate Decision

- UK: CBI Industrial Trends Orders (NOV)

- US: Initial Claims (Week ending Nov 14th)

- US: Philadelphia Fed Manufacturing Index (NOV)

- US: Existing Home Sales (OCT)

Friday

- Japan: Inflation Rate (OCT)

- Germany: PPI (OCT)

- UK: Retail Sales (OCT)

- Canada: New Housing Price Index (OCT)

- Canada: Retail Sales (SEP)

- EU: Consumer Confidence Flash (NOV)

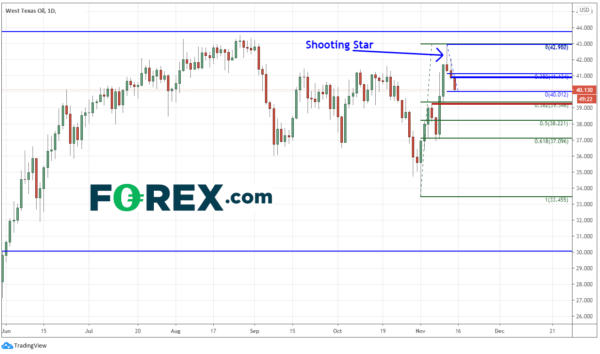

Chart of the Week: Daily WTI

Source: Tradingview, FOREX.com

Although West Texas Oil is up 12% for the month of November, the commodity appears to have run out of fuel. Fears of lack of demand from the increasing coronavirus cases caused WTI to pullback. On Wednesday last week, WTI put in a beautiful shooting star candlestick, which is a reversal candle. On Thursday and Friday WTI moved lower, closing near $40. There is strong support at $39.35, which is both the 38.2% Fibonacci retracement level from the November 2nd lows to the November 11th highs and horizontal support. Below there is the 50% retracement level at $38.22 and the 61.8% Fibonacci retracement level at $37.09. Short term resistance at $40.92, and the 38.2% Fibonacci retracement level from the highs of November 11th to Fridays lows, at $41.13.

This week may bring a Brexit deal; however, it may also continue to bring record setting coronavirus cases numbers along with it. Watch for more positive vaccine news as well.

Have a great weekend and please remember to always wash your hands!

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals