It’s going to be a relatively busy start to February as investors will be hoping the latest US jobs report will confirm that December’s rough patch was short lived. However, that won’t be the only data to test the market mood as preliminary GDP numbers out of the Eurozone could heighten fears of a double-dip recession. In the world of central banks, the first policy decisions of the year are due in Australia and Britain. The Reserve Bank of Australia meeting could be a bore while the Bank of England is expected to reveal the findings of its negative interest rates review. Also on the markets’ radar is the US Democrats’ attempt to bypass Republicans to approve Biden’s stimulus bill.

Aussie takes a knock but RBA to hold steady

The risk-sensitive Australian dollar has been on the receiving end of market jitters amid concerns of a stock market bubble and a possible delay to the next fiscal stimulus package in the United States. However, on the domestic front, not a lot has changed since the RBA last met in December 2020 and policymakers are not anticipated to announce any changes in their first review of the year on Tuesday.

The quarterly Monetary Policy Statement out on Friday might attract a bit more attention as investors will be interested to see how the Bank expects the economy to evolve over the next 2-3 years now that vaccinations are underway, and whether it is worried about the recently announced lockdowns in China – Australia’s biggest export destination.

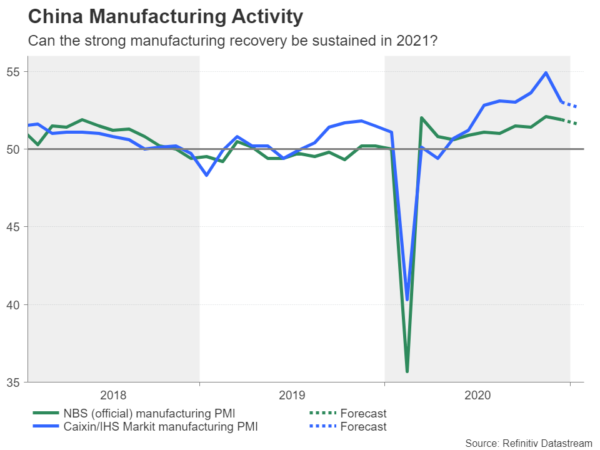

Economic indicators will include building approvals (Wednesday) and retail sales (Friday), though Chinese PMIs will probably matter more for the aussie. The official government manufacturing PMI is due on Monday, together with the Caixin/Markit PMI. Both are forecast to have eased slightly in January. A bigger-than-expected drop could dampen sentiment at the beginning of the trading week.

Across the Tasman Sea, fourth quarter jobs data will be the highlight for the New Zealand dollar on Wednesday.

Pound bulls hoping BoE will drop plan for negative rates

The Bank of England is expected to unveil its findings of its long-awaited study into the impact of negative rates on the banking sector when it meets on Thursday. The BoE is almost certain to stand pat on policy. But February is a ‘Super Thursday’ meeting, so the latest economic projections and a press conference by Governor Andrew Bailey, combined with the conclusions of the negative rates review, should make for an interesting day.

Recent remarks from policymakers, including from Bailey himself, suggest there is little appetite at the Bank to take rates into negative territory, at least not in the near term. However, while the odds for negative rates have diminished lately, it is unclear how the BoE will present its findings. Will it keep its options open even if the review does not promote the adoption of negative rates, or will it shut the door entirely on this experiment?

The pound could surge if the BoE were to rule out negative rates. Cable already has its sights set on the $1.38 level and cracking it would be an easy feat if investors further price out sub-zero rates.

However, negative rates will not be the only focal point for the British currency because the February Monetary Policy Report could contain downgraded growth forecasts. Most of the United Kingdom was placed into a full lockdown in January and the government has hinted the restrictions are unlikely to be relaxed before March. A pessimistic outlook and a dovish Bailey could offset any boost from negative rate plans being put on hold.

Eurozone GDP may add to euro’s woes

Another region suffering from fresh shutdowns is the euro area. Like the UK, continental Europe has been going in and out of lockdowns since November and the economic cost of those decisions will be laid bare on Tuesday when the preliminary estimate of fourth quarter GDP is reported. The Eurozone economy is forecast to have contracted by 1.8% in Q4, partially undoing the impressive rebound in Q3.

Much of this gloom is being put aside by investors as most are still hoping the recovery will go back into full steam in the second half of the year. However, concerns are growing about how the EU’s vaccine roll out is progressing as well as a renewed pursuit by the European Central Bank to exert downward pressure on the single currency. The EU has been hit by vaccine supply problems and a slow pace of distribution in many member states. Meanwhile, the ECB has been causing waves lately by hinting that rates have not yet reached the lower effective bound and launching an investigation into whether differences between ECB and Fed policy are to blame for the euro’s appreciation against the US dollar.

Hence, optimism for the euro area is looking a little shaky at the moment and a GDP miss could contribute to darkening the mood, though, following the better-than-forecast figures for Germany and France, a positive surprise is more probable. Other data worth keeping an eye on is Wednesday’s flash inflation print for January. Headline inflation is expected to return to positive territory after five straight months of falling prices. Although that would likely come as a relief for policymakers, it would be too soon to stop worrying about deflationary risks.

Can progress on stimulus ease Wall Street chaos?

It is not just bad earnings and virus fears that spark panic selling on Wall Street these days. Small retail investors have gone up against big hedge fund managers and institutional short sellers in a fight over the stock value of a struggling video-game retailer GameStop. The short squeeze brought on by a group of Reddit traders is threatening to bankrupt some hedge funds who suffered huge losses from their short positions when the stock soared.

But is this just a rare episode that will blow over in a few days or weeks or has it set a dangerous precedent that could shape Wall Street forever? Whichever way this saga is resolved, the effects are likely to ripple over at least into next week.

If that’s not enough to spur fresh volatility, then there’s plenty else that could, one of which is the bid by Democrats to bypass the Senate’s filibuster rule to push through President Biden’s $1.9 stimulus package. After the Republicans’ cold reception to Biden’s proposal, Democrats are having second thoughts about seeking a bipartisan compromise on the new relief package and may instead use the process of budget reconciliation to get the bill through Congress, which would avoid having to win over two-thirds of the Senate for approval.

Such a move could come as early as next week and would please equity markets if it means the stimulus legislation can be passed in its entirety without being watered down. Another potential sweetener for the markets is Friday’s nonfarm payrolls report.

Modest jobs rebound may disappoint, lift dollar

The US economy shed jobs in December for the first time since April as virus restrictions capped consumption. But the labour market is expected to have bounced back marginally in January, with forecasts of an increase of 20k in total non-farm payrolls. The unemployment rate is predicted to nudge up to 6.8%, however, underlining the slowdown in the recovery.

Other data that will provide more clues on the health of the economy are the ISM manufacturing and non-manufacturing PMIs on Monday and Wednesday, respectively, as well as factory orders on Thursday.

If the numbers fail to impress and broader sentiment does not improve, the dollar could extend its past week’s gains.

One of the biggest casualties of the greenback’s advances has been the Canadian dollar. Weaker oil prices and the stock market wobble have pushed the loonie to one-month lows. Friday’s employment report is unlikely to provide much support to the currency, however, as most of Canada remained in lockdown in January so there’s little prospect of the jobs market having improved during the month.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals