The European Central Bank will publish the minutes of its June 9-10 policy meeting on Thursday (11:30 GMT) as the Eurozone recovery gets into full swing. Policymakers struck a markedly dovish tone at their last gathering and although not all Governing Council members were happy about maintaining a “significantly higher pace” of bond purchases, the minutes will probably confirm that the hawks remain far outnumbered. The euro, which has been pummelled by the resurgent US dollar, could face some downside pressure from the minutes. But a bigger focus for the single currency in the near term is the outcome of the ECB’s strategy review, which could be announced very soon.

Wind blowing in ECB’s direction for once

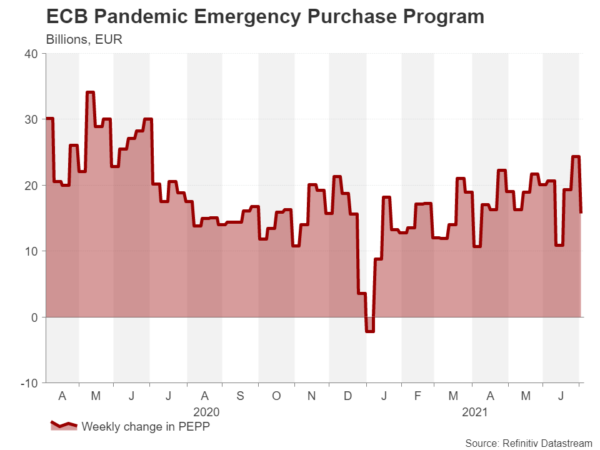

Altering the course of monetary policy isn’t a priority for the ECB right now. The pandemic emergency purchase programme (PEPP) isn’t due to expire until March 2022 so there is plenty of time to ponder the next move. Furthermore, the bond selloff has eased – in fact, bonds are back in demand and yields are falling. Lastly, the euro has weakened substantially lately as the Federal Reserve looks set to beat the ECB in tapering first. All the above mean the ECB can more than afford to take its time before having to decide if or how the PEPP will be extended.

There is one niggle, however, that will almost certainly be playing on policymakers’ minds in the next meeting or two and that is the current pace of asset purchases. In March, the ECB stepped up its bond buying scheme not only to curb an unduly jump in euro area yields but to also repair the damage after sending the wrong signal to the markets by slowing the pace too much earlier in the year.

But the accelerated pace of purchases may soon have to be pared back as, apart from the strengthening economic rebound, there seems to be revived demand for government bonds and soaring yields no longer pose a problem for the Eurozone recovery. Besides, the move was meant to be temporary and now that it is almost certain the Fed will begin to wind down its stimulus over the coming months, the ECB is in a position to take its own foot off the pedal slightly.

Hints of slower purchases might support euro

The June minutes might shed some light as to how strongly policymakers feel about dropping the pledge to conduct the PEPP at a “significantly higher pace than during the first months of this year” as early as the July meeting.

Any such hints would be positive for the euro, which is really struggling at the moment to hold above the $1.18 level. If the ECB clearly signals that there may no longer be a need for accelerated bond purchases, euro/dollar could rebound above the 61.8% Fibonacci retracement of the March-May uptrend at $1.1917.

However, should policymakers provide no timeline of when asset purchases might need to be reduced, the pair could slip below the critical $1.18 barrier and head towards the March trough of $1.1702.

Strategy review could be key to exiting pandemic QE

In the bigger scheme of things a change to the PEPP pace is a minor detail and a much more important decision looming is the one about overhauling the ECB’s monetary policy strategy. Some reports indicate an announcement is imminent amid “good progress” at recent discussions held by the Governing Council at a Frankfurt hillside retreat. But whether the outcome is unveiled over the next few days or weeks, the ECB is unlikely to make a major policy change before the strategy review is completed.

The review could see the ECB’s unusual inflation objective of “below, but close to, 2%” being ditched for a more symmetrical target of around 2% used by most other central banks. One other option is to follow the Fed in adopting average inflation targeting, though it’s unlikely hawkish governors such as those of Germany, Austria and the Netherlands would ever approve of this.

Defining inflation overshoot

Either way, President Christine Lagarde will soon have to clarify how much of an inflation overshoot the Bank is willing to tolerate and for how long. Inflation in the euro area – while on the rise – has yet to shoot up to levels such as those in the United States. But it might not be long before it does.

This makes the timing of the strategy review all the more important as it could determine how quickly asset purchases are scaled back. The other potential revamp that could have major repercussions on how policy is set is whether the ECB will decide to look at different measures of inflation, possibly even launching its own price index.

There is a growing debate about the need to include house prices into Eurostat’s Harmonised Indices of Consumer Prices (HICP). But even if the ECB were to push for a new inflation metric that incorporates housing and other costs, it could take several years to develop a new price index so there might not necessarily be any near term policy implications from this.

Can the Eurozone avoid the Delta carnage?

Amidst all the upcoming policy reviews and decisions, there is another thing investors should keep an eye on – the Delta variant. Some Eurozone nations like Spain appear to be headed in the direction of the UK, with new infections surging in recent days, driven mainly by the highly contagious Delta strain. Should the Delta outbreak worsen across Europe in the coming weeks, it could scupper plans to fully reopen shuttered sectors of the economy, which would ultimately delay any tapering plans by the ECB.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals