The next seven days will be an important one for the US dollar as high-level US-Sino trade talks, the policy meeting by the Federal Reserve as well as key data releases will likely determine the currency’s next turn. The Australian dollar will also be in focus as inflation and other closely-watched indicators will be on the agenda, while in the Eurozone, flash GDP estimates could exert more negative pressure on the beleaguered euro.

Aussie vulnerable from Australian inflation and Chinese PMIs

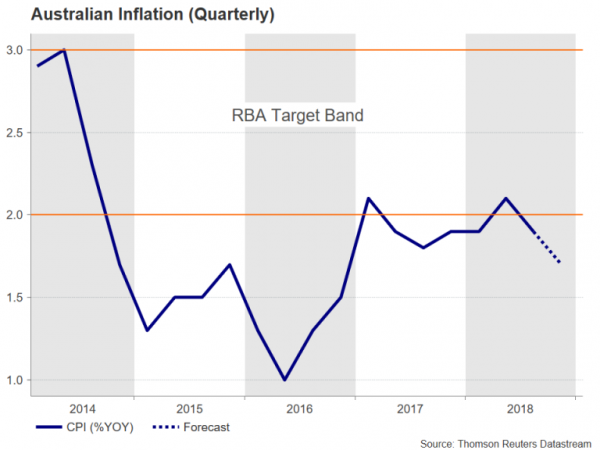

The Australian dollar posted some significant losses this week on rising expectations that the Reserve Bank of Australia could cut rates later this year. Any signs of weakness therefore from the raft of data due from Australia and China could put the aussie back on a negative footing. First on the horizon are Chinese industrial profits for December on Monday, followed by the National Australia Bank’s business confidence gauge on Tuesday, also for December.

The highlight will be Wednesday’s inflation report for the fourth quarter out of Australia. The quarterly rate of CPI is forecast to have risen by 0.4% in the final three months of 2018, which would produce an annual rate of 1.7%. If confirmed, this would represent a 0.2 percentage points slowdown from the prior quarter and a further deviation from the RBA’s 2-3% target band.

The inflation theme will continue on Thursday and Friday with the release of export prices and the producer price index, respectively, both for the fourth quarter. Private sector lending figures are also out on Thursday, along with China’s official manufacturing PMI. The Caixin/Markit manufacturing PMI will follow suit on Friday. Both indices are forecast to slip further into negative territory in January, underlining the weakening picture in the world’s second largest economy.

Japanese economy to remain under the spotlight

After the BoJ meeting and worse-than-expected export numbers this past week, investors will be watching retail sales, industrial output and unemployment figures for December for clues on whether the slump in manufacturing is becoming broader based. Retails sales and industrial production are up first, with the job numbers coming up on Friday.

The yen is unlikely to see significant action from the data, but traders could respond to Thursday’s Summary of Opinions of the Bank of Japan’s policy meeting held during the past week. The Bank lowered its forecast for inflation and the Governor, Haruhiko Kuroda, warned of growing downside risks at his press conference. Should the Summary reveal even deeper concerns by other board members about the worsening outlook, the yen could face some downside pressure.

More pain, no joy from Eurozone GDP data

The euro slipped to a 5-week low of $1.1286 on Thursday as ECB President, Mario Draghi, answered reporters’ questions at the bank’s post-meeting press briefing. Draghi acknowledged for the first time that “the risks surrounding the euro area growth outlook have moved to the downside”. His downbeat remarks will likely bring next week’s releases under intense scrutiny, especially the GDP estimates.

But first on the Eurozone calendar is the economic sentiment indicator on Wednesday. The index is forecast to drop to a fresh two-year low in January, in further evidence of deteriorating conditions in the euro area. On Thursday, the first estimate of GDP growth for the fourth quarter will be attracting headlines. The Eurozone economy is projected to have expanded by lowly 0.2% quarter-on-quarter. This would be unchanged from the prior period but would bring the annual rate down to just 1.2%. A lower-than-expected reading could pull the euro to fresh lows versus the greenback and possibly threaten the $1.12 handle. In addition to the Eurozone-wide numbers, investors will also be watching France’s and Italy’s growth estimates on Wednesday and Thursday, respectively, as there are concerns that the two economies are headed for contraction in the first quarter and Italy could already be in recession.

Last but not least, the flash inflation readings for January will be important too. Headline inflation in the euro bloc is expected to ease further in January to 1.4% year-on-year.

Pound bulls pin hopes on EU Withdrawal Bill amendment

UK lawmakers will vote on Theresa May’s ‘Plan B’ on Tuesday, setting the stage for another showdown with the government. However, with Plan B looking very much like Plan A, MPs will be rushing to pass amendments to the bill, some of which are aimed at blocking a crash exit from the EU. If none of the amendments pass and the deal is rejected, pound bulls could be set for large losses, with cable probably sharply reversing some of its recent gains, having rallied above the $1.31 level this week.

Away from the Brexit saga, the Markit/CIPS manufacturing PMI will be monitored on Friday.

Trade talks, Fed and nonfarm payrolls to take centre stage

Worried traders will be hoping for more soothing words from Fed Chairman, Jerome Powell, on Wednesday when he holds his first post-meeting press conference for 2019. US data will also be on the radar with a flurry of economic indicators scheduled for release, though some like the advance GDP estimate for the fourth quarter and PCE inflation print for December will likely be delayed due to the ongoing government shutdown.

Not affected by the shutdown is the January jobs report on Friday, but ahead of that there’s plenty of other January data to draw traders’ attention. Among which, the more notable releases are the Conference Board’s consumer confidence index on Tuesday, the ADP employment report on Wednesday, the Chicago PMI on Thursday, as well as the ISM manufacturing PMI soon after the NFP numbers on Friday.

Given the concerns about the US housing market, Tuesday’s S&P CoreLogic Case-Shiller house price index for November and Wednesday’s pending home sales for December will be looked at too.

The week’s focal point, however, will be the next round of US-China trade discussions on Wednesday/Thursday, and the FOMC meeting on Wednesday where the Fed will make its first policy statement since the shift to a more “patient” mode. China’s Vice Premier Liu He will be in Washington hoping to find a way to resolve the ongoing trade row. The absence of substantial progress in the talks could spark another bout of risk aversion, which would boost the greenback.

As for the Fed gathering, no change in policy is expected and there are no economic projections for the January meeting but starting this month, all meetings will be followed with a press conference, so the dollar will likely be highly sensitive to remarks by Powell on the growth outlook.

Friday’s jobs report could also prove market moving, but based on the forecast, nothing dramatic is being anticipated. The US economy is predicted to have created 183k jobs in January, slowing from December’s 312k surge. A smaller number could raise concerns about the impact of the government shutdown. The unemployment rate is forecast to hold at 3.9%, while average hourly earnings are expected to have risen by 3.2% y/y in January, unchanged from the prior month.

For traders: our Portfolio of forex robots for automated trading has low risk and stable profit. You can try to test results of our download forex ea

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals