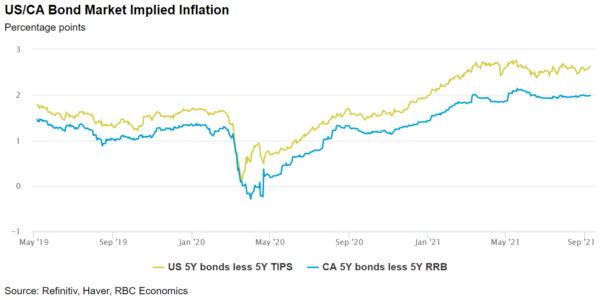

Inflation reports will steal the spotlight next week, with annual Canadian price growth expected to climb to 4% in August compared to a year ago—the fastest pace since 2003. But much of that rise is from very low levels last year, when tighter COVID restrictions were in place. These so-called “base effects” also explain why Canada’s CPI was up 3.7% year-over-year the prior month. Strip them away and CPI appears more normal, growing at an annualized 2.1% in July compared to pre-pandemic February 2020 levels. The dynamic is also likely why the BoC has characterized much of recent CPI increases as ‘transitory.’ Still, recent reports have shown a broadening in price pressures. Prices for autos have been driven up by supply chain disruptions. Shelter prices have risen rapidly too, though will likely slow as resale markets come off the boil and lumber prices drop.

Meanwhile, we expect U.S. inflation to hold at 5.4%, even as monthly price growth eases. And across both countries, there’s little to suggest long run inflation expectations are coming undone. Bond market pricing shows expectations were relatively stable in recent months, though pent up demand for services may push prices higher. To be sure, signs of (broadly-based) price growth above pre-pandemic trends would be harder to dismiss as ‘transitory’. And the demand growth that would generate that kind of inflation pressure depends on the virus. Over 85% of eligible Canadians are now at least partially vaccinated. But the threat of COVID is not gone, and the economy is far from fully recovered. Monetary policymakers will be in no hurry to pull back on stimulus even if inflation continues to overshoot the 1% to 3% target range for a few more months.

Week ahead data watch:

- Statscan’s preliminary estimates for Manufacturing and Wholesale sales both pointed declines in July (-1.2% and -2.0%, respectiely). Both likely reflected in part sharply lower lumber prices, which fell more than 20% in July.

- US CPI inflation is expected to remain sharply elevated on a year-over-year basis at 5.4%. However focus will be on month-over-month growth for signs of further moderation after slowing to 0.4% from an average of 0.7% the prior three months.

- Solid permit issuance is expected to continue to support elevated levels of Canadian housing starts (275k) in August.

- We look to see US retail sales to record another decline of 1% in August on account of lower auto sales.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals